Government spending and inflation are sending long-term yields higher across the developed world. Will the 30-year Treasury yield 6% in a year?

Bond yields rose this month to levels that are setting off alarm bells across financial markets. The 30-year U.S. Treasury bond yield hit 5.20% on May 19, the highest level since mid-2007, just before the 2008-09 financial crisis. The 10-year yield topped 4.68% the same day before retreating, but remains above 4.50%.

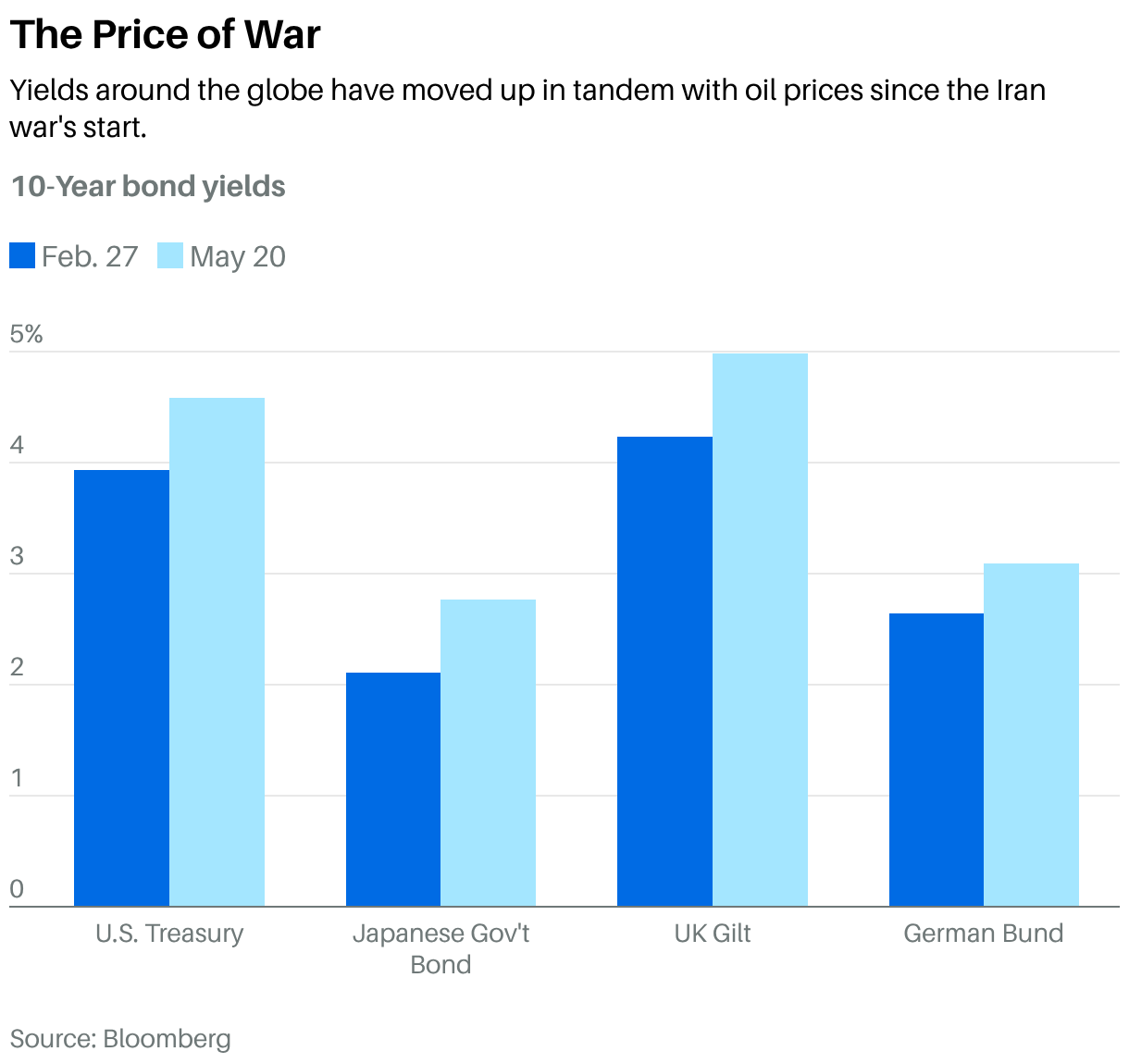

The trend is global: Yields on United Kingdom gilts, German Bunds, and Japanese government bonds have also been climbing, in tandem with a rise in crude-oil prices since the Iran war began in late February. But these are just the latest moves in a sustained rise in yields that has been under way since long-term interest rates bottomed at historic lows in 2020, during the worst of the Covid pandemic.

What is different this time is that long-term interest rates have reached levels that could put pressure on equity valuations. Major stock indexes are just below historic highs, reflecting investor enthusiasm about artificial-intelligence plays, which could reach a fever pitch as some of the biggest AI developers prepare to come public. Higher bond yields provide competition for stocks, and raise corporate borrowing costs.

The proximate cause of the recent bond rout—bond prices move inversely to yields—is the rise in oil prices due to the continuing closure of the Strait of Hormuz, a critical energy-shipping waterway in the Middle East. West Texas Intermediate, the U.S. benchmark crude, nearly doubled to just shy of $113 a barrel on April 7 from about $67 a barrel on Feb. 27, the day before the war began.

Crude prices have since retreated to the low-$100s, but even at lower levels they’re creating inflationary pressures that may not dissipate soon.

Robin Brooks, senior fellow at the Brookings Institution and former chief economist at the Institute for International Finance, cites three reasons for the rise in bond yields, which has lifted the 10-year Treasury yield from about 0.50% in 2020: Governments almost everywhere went on an emergency borrowing binge to counter the economic impact of the pandemic. There has been no meaningful reduction in deficits since then. And, inflation has remained higher and more volatile than in the years preceding Covid.

Total U.S. federal debt held by the public topped 100% of GDP in this year’s first quarter, approaching the record of 106% after World War II. The Congressional Budget Office estimates that the budget deficit will total 5.8% of GDP in 2026. More important is the future trajectory: The CBO estimates that the U.S. budget deficit will average 6.1% of GDP annually over the entire decade through 2036—far higher than the 3.8% average of the past 50 years.

A fraught geopolitical environment is pushing up military spending, which means many countries may have to issue still more debt. Buyers are likely to demand even higher yields. The Trump administration is seeking a 44% jump in military expenditure for fiscal 2027, to a record $1.5 trillion. Other countries, notably America’s European allies and Canada, boosted their military spending by more than 20% in 2025 and pledged to scale up military and security-related expenditure to 5% of GDP by 2035.

An even bigger burden on budgets is the seemingly intractable increase in interest expense from the past borrowing binge. Interest expense is running at more than $1 trillion annually in the U.S., topping current military outlays (for now).

As for inflation, it has fallen from recent peak levels in 2022, but remains elevated and volatile. As a result, central banks have had to implement more frequent and larger hikes in short-term interest rates to contain expectations for future inflation.

The futures market now sees a 70% chance of a Federal Reserve rate hike of at least one-quarter percentage point by December, according to the CME FedWatch tool. That marks a notable change from prior expectations of more than two quarter-point cuts by the Fed by year end.

J.P. Morgan economists look for the European Central Bank and the Bank of Japan to raise their policy rates in June, with a possible hike from the Bank of England.

When government borrowing costs top the growth of nominal GDP, or an economy measured in current dollars, including inflation, that’s another danger signal, say Brown Brothers Harriman’s currency analysts. That has already happened in the U.K., with the 10-year gilt yielding nearly 5%, above annual 10-year nominal GDP growth of about 4.8%.

Even more perilous is the crossover in Japan, where the 10-year government yield has soared to more than 2.50%, the highest level since mid-1997, after years of artificially suppressed interest rates there. Japan’s 10-year average annual nominal GDP growth is 1.9%.

What happens in overseas bond markets doesn’t stay there, however. “For years, foreign investors, starved for yield at home, exported capital into U.S. Treasuries,” stated a recent Yardeni Research note, “As domestic yields abroad rise, that incentive weakens. The U.S. government must compete for buyers of its debt on its own merits in a world of high government deficits and rising inflation.”

The U.S. Treasury has attempted to limit its interest costs by twisting its borrowing toward short-term bills and away from intermediate- and long-term notes and bonds, which carry higher yields. That ploy, initiated in 2022 by former Treasury Secretary Janet Yellen, was criticized then by now–U.S. Treasury Secretary Scott Bessent, who nonetheless continued it as her successor.

The practice worked in Uncle Sam’s favor, as the Fed lowered its short-term interest rate target by 1.75 percentage points in 2024 and 2025, but it may backfire if the central bank starts hiking.

In the near term, bond yields will continue to be driven by progress, or lack thereof, in resolving the Iran war and reopening the Strait of Hormuz. Given the proximity of the U.S. midterm elections and the importance of gasoline prices to voters, markets have priced in a reversal in the rise in oil. But even if that comes to pass, inflation excluding food and energy remains sticky, notably for services.

Longer term, the debt overhang will remain throughout the developed markets. There is little prospect of governments reining it in while they borrow to fund domestic spending and ramp up military expenditure. Plus, the AI spending boom will add to corporate borrowing.

Reflecting these trends, 62% of respondents to Bank of America’s most recent fund-manager survey indicated they anticipate the 30-year Treasury yield will top 6% in the next 12 months. That sort of surge would almost certainly send stocks reeling, which could make for a rally in bonds. But it would be short-lived.

Write to Randall W. Forsyth at randall.forsyth@barrons.com