Treasury inflation-protected securities are generating positive returns despite a rough bond market.

Inflation is rising, bond prices are falling, and TIPS are having their moment.

The prospect of a protracted period of elevated inflation—stemming from higher oil prices and other factors—heightens the appeal of Treasury inflation-protected securities. TIPS are among the only bonds that can insulate investors from higher inflation.

While most bonds have dropped in price this year, TIPS have generated positive returns. And they remain attractively priced.

“TIPS are, I think, probably one of the most underappreciated and underutilized investments. It’s like a Treasury, but it has an inflation hedge,” Alex Shahidi, managing partner and co-chief investment officer of Los Angeles–based Evoke Advisors, told Barron’s Advisor.

Not enough individual investors and financial advisors include TIPS in their bond allocations. That’s a mistake.

It has been a rocky period for the bond market, with 10-year Treasuries recently hitting a yield of almost 4.7%, their highest since January 2025. Bond prices go down when yields go up.

TIPS are like insurance, offering investor protection against higher inflation. The yield on TIPS has two components: The bonds pay investors the inflation rate, as measured by U.S. consumer prices, plus a bonus, or real, yield above inflation that ranges from one to almost three percentage points depending on maturity.

Here’s the calculus for someone considering a 10-year Treasury investment. The regular Treasury 10-year note yields 4.60%, while 10-year TIPS have a real yield of 2.15%. That means inflation has to run at more than 2.45% (4.60% minus 2.15%) for TIPS to be the superior investment over the next 10 years.

That sounds like a good bet. April consumer prices rose 0.6% from March and at 3.8% over the prior 12 months. Analysts see a good chance of 3%-plus inflation for the rest of 2026—above the Federal Reserve’s target of 2%. Then there is the insurance aspect. TIPS effectively provide insurance against higher inflation, while regular Treasuries and most bonds don’t.

Long-term TIPS have the highest yields and offer an appealing stand-alone investment.

The real yield of almost 3% on 30-year TIPS is near a high in the nearly 30 years of TIPS issuance. Pension funds, endowments, and other tax-exempt portfolios often try to generate annual returns over time that are at least five points higher than inflation and make risky investments such as private equity to try to achieve that.

Investors can effectively get something close to that—a 3% real yield on Treasuries with no risk. This assumes the government doesn’t default. The break-even inflation rate on 30-year TIPS is just 2.3%, enhancing their appeal.

“With 30-year TIPS now yielding almost 3% real, investors can now lock in inflation-adjusted returns competitive with traditional portfolios without the risks that come from a large slug of equities,” wrote Bob Elliott, CIO of Unlimited Fund and a former Bridgewater Associates manager on X last week.

Most investors focus on shorter-maturity TIPS due in 10 years or less. They offer inflation protection and carry less price risk than long-term issues.

What are the risks with TIPS? If inflation cools, demand may ease and TIPS could underperform U.S. Treasuries. And if inflation does move much higher, TIPS probably will best regular Treasuries, but they still could generate negative returns.

There are more than $2 trillion of TIPS outstanding, and investors can buy them in several ways.

They can be purchased directly from the Treasury at regular auctions of TIPS of bonds with five-year, 10-year and 30-year maturities. They can be bought in the secondary market through banks and brokers. The Treasury auctioned 10-year TIPS this in mid-May and plans to sell five-year TIPS in June.

Funds, particularly low-fee exchange-traded funds from a range of issuers, offer a good alternative to individual bonds by simplifying some of ownership mechanics.

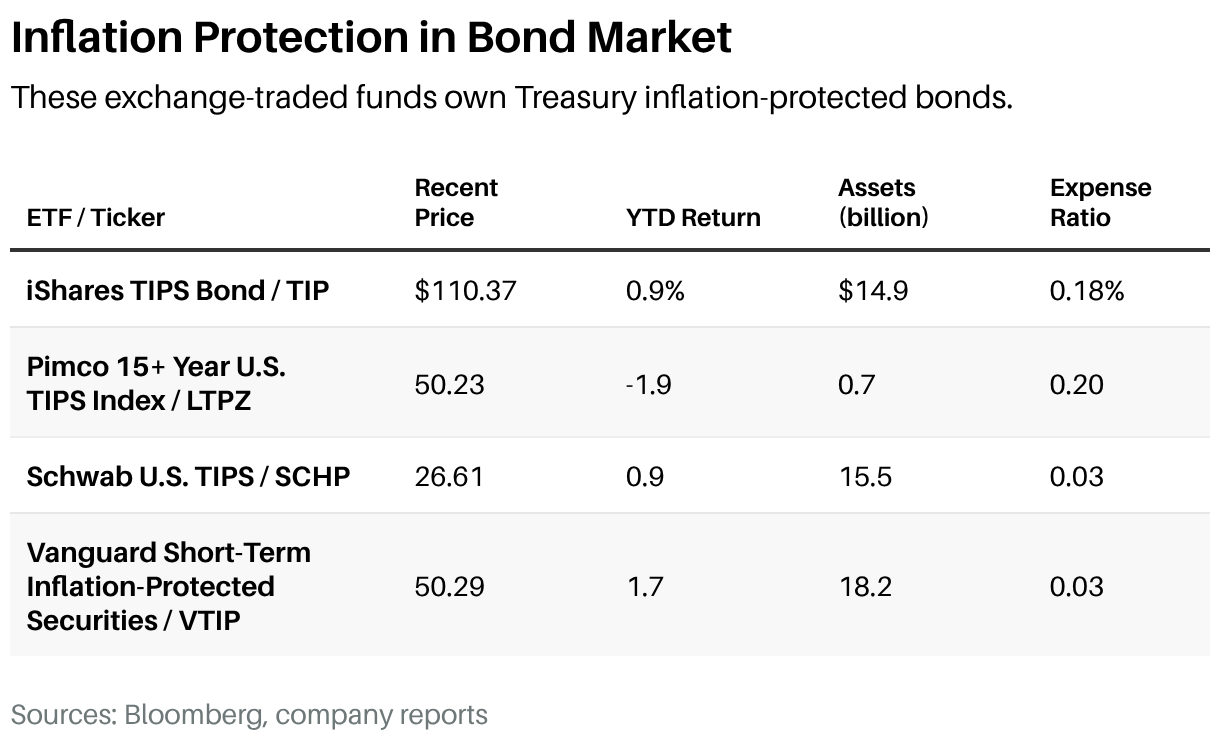

The four largest TIPS ETFs are the $18 billion Vanguard Short-Term Inflation-Protected Securities, the Schwab U.S. TIPS, the iShares 0-5 Year TIPS Bond, and the iShares TIPS Bond. The final three funds are each about $15 billion in size. Fees are low, including just 0.03% on the iShares 0-5 Year TIPS ETF, the Vanguard ETF, and the Schwab TIPS ETF. The Vanguard ETF is a share class of the larger $68 billion Vanguard Short-Term Inflation-Protected Securities mutual fund. The Pimco 15+ Year U.S. TIPS Index ETF offers exposure to long-dated bonds.

Investors can create a maturity ladder of TIPS, and iShares simplifies that with its iShares iBonds 1-5 Year TIPS Ladder ETF. The TIPSLadder.com website gives you the bond details to construct your own ladder.

Vanguard includes TIPS in some of its shorter-dated target-date mutual funds geared toward investors around retirement age.

There are some quirky aspects to TIPS. The inflation component of the yield is added to the principal every six months, and the real rate is paid in cash.

This results in a phantom income issue because investors owe federal income taxes on the inflation component (Treasury interest is exempt from state and local taxes) and get no cash. The ETFs pay out that inflation-related interest, avoiding this issue.

Another way to buy inflation-protected Treasuries is through Series I U.S. savings bonds offered through the Treasury.gov website. They now offer a yield of nearly one percentage point above inflation. The current rate—lasting through the end of October—is 4.26%. The rate gets reset every six months based on the consumer-price-index inflation figure.

With certain exceptions, investors are limited to $10,000 a year in I bond purchases. They need to be held for at least 12 months, and sales within five years result in a loss of three months’ worth of interest. I bonds mature in 30 years and have a nice tax attribute. Taxes on interest, which is added to principal every six months, can be deferred until maturity, giving I Bonds an individual-retirement-account-like character.

With inflation heading higher, TIPS are an underappreciated and underowned asset class that merits greater attention from investors.

Write to Andrew Bary at andrew.bary@barrons.com