Active funds such as Oberweis Micro-Cap and Diamond Hill Small Cap could have an edge as trends shift in favor of smaller stocks.

You have to admire Dimensional Fund Advisors’ timing. In March, the money manager launched the U.S. Micro Cap Portfolio, an exchange-traded fund version of a top mutual fund previously available only to financial advisors.

Luckily for investors, microcap stocks have recently been on a tear.

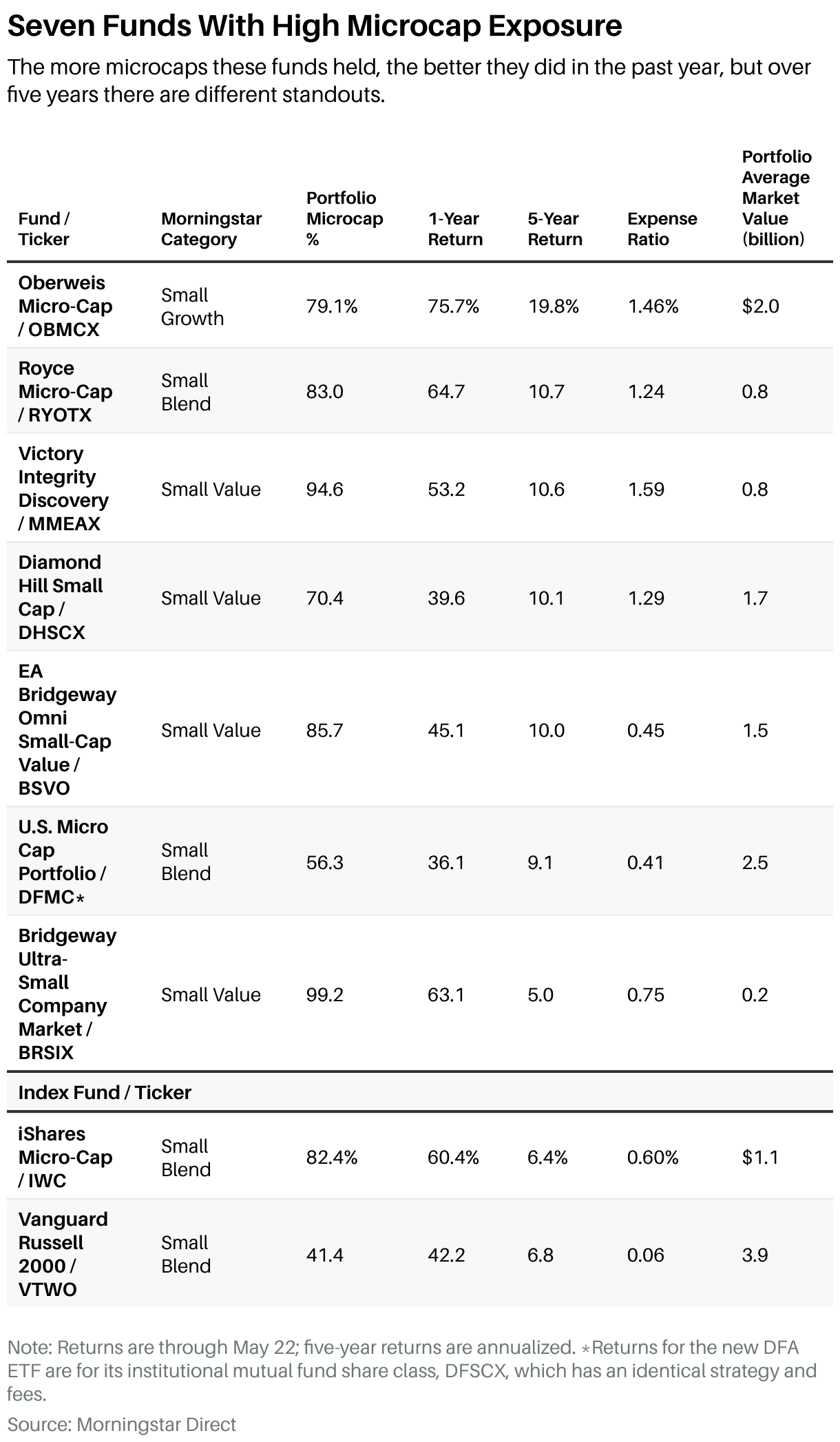

After five straight calendar years of underperformance, small-cap stocks are finally beating large ones. And the smallest of the small—microcaps—are doing even better. In the past 12 months, the Vanguard Russell 2000 ETF has gained 42.2% versus the Vanguard S&P 500’s 29.5%. But iShares Micro-Cap has surged 60.4%, and Bridgeway Ultra-Small Company Market—which invests in the tiniest of all companies—is up 63.1%.

The rally began when the tariff panic ended in April of last year, says Francis Gannon, co-chief investment officer of Royce Investment Partners, a small-cap-focused money manager. “When you see small-caps outperform like this, they tend to outperform for a decade,” he says.

Gannon says a reshoring of businesses since the trade war began has benefited smaller companies more than large multinational ones. He also thinks favorable tax policy that allows “100% depreciation on research and capex [capital expenditures] is really driving a lot of what you’re seeing from a small-cap earnings perspective.” The power of these trends is amplified as one goes down the capitalization ladder to the smallest microcaps.

Defining what microcaps are can be tricky, though. There is no official microcap fund category at Morningstar, but the research firm historically has defined microcap stocks as the smallest 3% of companies by capitalization in the market. For its U.S. Micro Cap Portfolio, DFA defines microcaps as the smallest 5%. At the end of 2025, that meant companies with a market cap below $6.8 billion—an outlier upper limit, as the average microcap in the ETF’s portfolio is currently $2.5 billion. Some of its holdings are as small as $200 million.

Because of those definitional differences, Morningstar categorizes 40% of DFA’s portfolio as small-cap and 56% as microcap. Microcaps have “a squishy definition,” admits Dan Sotiroff, an associate director at Morningstar. Yet he still rates the DFA fund “Gold” for its well-designed strategy. Like most DFA quantitative funds, this one successfully straddles the line between active and index-fund management, holding 1,731 stocks but eliminating unprofitable and highly-valued ones. It has beaten the iShares Micro-Cap and the Vanguard Russell 2000 index ETFs over the past five-, 10-, and 15-year periods.

Still, microcap purists may want to consider Bridgeway Ultra-Small Company Market—which is also quasi-indexed—as its portfolio has an average market cap of only $250 million versus DFA’s $2.5 billion, iShares Micro-Cap’s $1.1 billion, and the Vanguard Russell 2000’s $3.9 billion.

There is a strong case, though, for active management. “Microcaps, in particular, are a highly inefficient asset class,” Gannon says. “There’s no analyst coverage” for many microcap companies.

Morningstar’s research on active versus passive funds shows better odds of outperformance for active managers in small-caps. For microcaps, in particular, there have been a handful of active funds, such as Oberweis Micro-Cap, Royce Micro-Cap, and Diamond Hill Small Cap—which has 70% of its portfolio in microcaps—that have beaten their benchmarks by a wide margin.

Notably, these are mutual funds, as it’s hard to have the liquidity to run an active microcap ETF like DFA’s without owning hundreds of stocks. Royce Micro-Cap owns 157 stocks versus DFA’s 1,731, and that allows its co-managers to home in on tiny, undiscovered artificial-intelligence plays like Adtran, which provides fiberoptic network and communications equipment necessary for AI hyperscalers.

Oberweis Micro-Cap currently holds 80 stocks, and Diamond Hill Small Cap, 57. Diamond Hill manager Aaron Monroe likes companies that dominate the supply of “picks and shovels” niche components. Lately these businesses have been in healthcare, such as UFP Technologies, which makes components for medical devices. “Boring is beautiful,” Monroe says.

The returns for microcaps are more interesting.

Write to editors@barrons.com