Fee pressures from low-cost index funds have driven many mergers in recent years as active managers need scale—and reduced head counts—to compete.

Even in this era of index investing, the news that 25 Franklin Templeton managers would be accepting buyouts and leaving the fund company is unsettling.

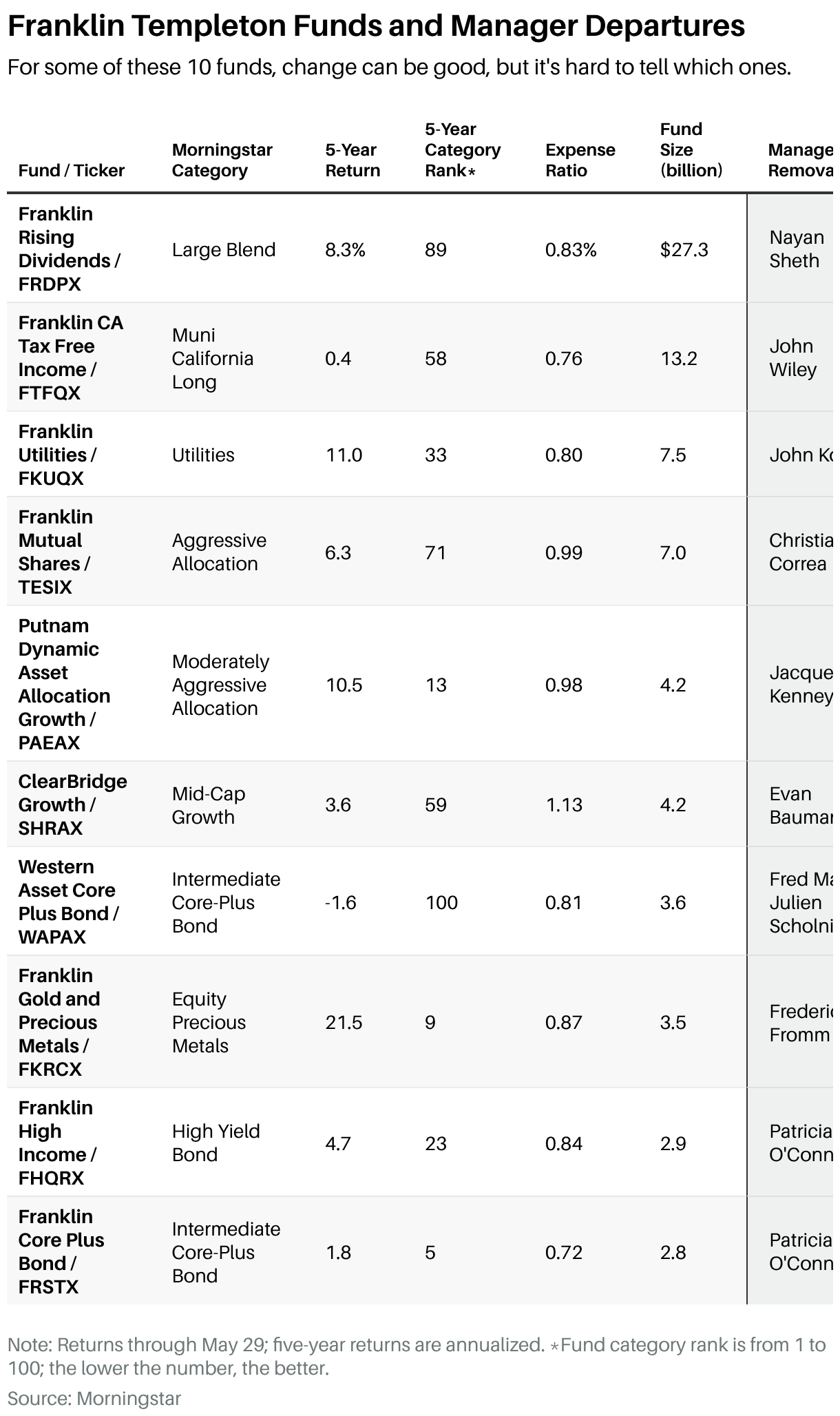

Investors once treated big fund-shop managers as celebrities, and the departure of ones at former mainstays such as Franklin Rising Dividends, Franklin Mutual Shares, Franklin High Income, and Western Asset Core Plus Bond would’ve made headlines.

“The number and the kind of departures announced here certainly stood out compared to what you usually see, which rarely affects investment teams,” says Max Curtin, a senior analyst at Morningstar who covered the Franklin departures, which were announced in April.

For investors, the sudden departure of a longtime manager triggers the question: Should I stay or should I go? Though one’s first inclination might be to flee, the reason for a manager’s departure should influence one’s ultimate decision.

“The disruption that comes with the change of management, and then potentially a coinciding change in strategy or philosophy—that’s in most cases negative,” Curtin says. “But if something’s not working, if [the fund’s] underperforming, maybe we should view change as good.”

A manager of a top-performing fund jumping ship to start his own fund or join a rival fund company is often, although not always, a sell sign. Famously, bond manager Jeffrey Gundlach, dubbed the Bond King, founded DoubleLine Capital funds in 2009 after being fired from TCW Total Return, taking 14 members of his TCW investment staff with him. Many of the fund’s investors followed him. TCW changed his former charge’s name in 2024 to TCW Securitized Bond, and it’s now a poorly rated fund.

Equally famous bond manager Bill Gross left Pimco Total Return to join Janus Funds in 2014, with little subsequent damage to the Pimco fund. Notably, Gross didn’t take his Pimco analyst staff with him. At big fund shops, those analytical resources often matter more than the manager.

Last year, for instance, T. Rowe Price replaced manager Josh Spencer with Shaun Currie at T. Rowe Price New Horizons, which has been lagging in recent years and bleeding assets, from a 2021 peak of $43.8 billion to $14 billion today. But remaining investors may want to wait for a turnaround as the fund’s mid-cap growth strategy and the analytical team backing it are the same.

“There’s a lot of resources surrounding [Currie], and he’s utilizing those resources,” says Josh Nelson, T. Rowe’s head of Global Equity. “From a retail investor’s mind-set, you’re buying New Horizons and it’s still very similar.” T. Rowe has a staff of 905 investment professionals, which includes 352 research analysts. Yet the shift was enough that Morningstar downgraded the fund’s People and Process ratings from above average to average, as Currie is untested in the role.

By contrast, Morningstar’s analysts have more confidence in T. Rowe Price Mid-Cap Growth. They still rate it Silver overall even after lead manager Brian Berghuis retired at the end of 2025 with one of the fund category’s strongest records since he took over the fund in 1992. T. Rowe designed a careful succession plan for Berghuis, appointing associate managers Ashley Woodruff and Don Easley in 2020 and promoting both in 2025, with Woodruff becoming lead manager last September. The two also have 30 dedicated analysts supporting them.

In Franklin Templeton’s case, the managerial shifts are largely due to investment team consolidation after the company acquired other investment managers such as Legg Mason in 2020 and Putnam Investments in 2024. Fee pressures from low-cost index funds have driven many such mergers in recent years as active managers need scale to compete, and, as it turns out, a reduced head count.

Regarding the latest round of departures, Franklin Templeton’s Jeaneen Terrio declined to call it consolidation, instead citing the need “to streamline the business for efficiency and look for the best ways to serve clients going forward.” The departures represent less than 5% of total public markets investment staff, she adds.

Such shifts highlight the challenges publicly traded asset managers like Franklin face when balancing the imperatives of maximizing shareholder value and protecting the interests of fund investors, Morningtar’s Curtin says. Pressure to protect profitability can influence personnel decisions.

One indication that Curtin is right is that Terrio says there are no current plans to reduce fees for Franklin funds facing manager departures. If the goal of reducing head count was to serve Franklin’s end clients instead of its management company’s shareholders, the cost savings would be passed on to fund investors via lower expenses.

Still, some of the shifts at Franklin could prove beneficial, or at least neutral. Three different underlying equity analyst groups—Franklin Equity, Mutual Series, and Brandywine—merged at the end of 2025. That provides a larger total pool of analysts for the remaining co-managers, Matthew Quinlan and Amritha Kasturirangan, of the $27 billion Franklin Rising Dividends fund after Nayan Sheth left this May.

Quinlan and Kasturirangan plan to rely more on the expanded analyst pool. Since this fund has lagged behind 89% of its fund-category peers in the past five years and 88% in the past 15, it’s hard to imagine these managerial changes will make things worse.

Still, any dramatic style or portfolio shifts that result could spook investors, even if changes prove beneficial. One underrated benefit of indexing is consistency. With an S&P 500 fund, you know exactly what you’re getting.

Write to editors@barrons.com