Philipp Navratil aims to restart growth in the 160-year-old food giant by focusing on core brands like KitKat, Fancy Feast, and Nespresso.

ROMONT, Switzerland—Willy Wonka would have marveled at one of the machines at a manufacturing plant here—a contraption that injects flavors into coffee capsules via a set of whirring tubes labeled “hazelnut,” “caramel,” and “blueberry cheesecake.”

This isn’t one of Roald Dahl’s fictional chocolate factories, although KitKat and Nesquik owner Nestlé runs plenty of those. The aroma tipping station can be found at a Nespresso plant located a 30-minute drive north from Nestlé’s head office in Vevey, where high-speed filling machines deliver more than 1,000 instant-coffee pods a minute. Even the lobby and elevators smell of roasted coffee, although workers say they stop noticing after a while.

Most Nestlé employees, no matter their department, tour one of the company’s 335 factories as part of their induction. Manufacturing is at the heart of everything the world’s largest food company is doing as it tries to revive its shares following a bruising spell. The Swiss-listed stock has plummeted 41% since early 2022, dragged down by weak sales, misguided acquisitions, and a revolving door at the top. The nadir came in September 2025, when the 160-year-old conglomerate hired its third CEO in just 13 months.

Nestlé is trying to end the slump by winning back market share and slimming down its sprawling business. CEO Philipp Navratil’s challenge is to revive sales, trim fat from a business that has strayed beyond its core brands, and bring stability after years of turmoil. Early signs suggest the turnaround plan is starting to work, with a fresh focus on the coffee pods, pet food, and the chocolate bars that Nestlé makes at factories like this one.

“Selling more portions, more cups, more servings every day…will solve most of our issues from the past,” Navratil tells Barron’s.

The KitKat Heist

In March, Nestlé showed that it’s adroit enough to bounce back from some bad luck. When thieves snatched 12 metric tons of KitKats in transit from Italy to Poland, the company capitalized with some free publicity for one of its most famous brands.

Rather than putting out a dry statement promising to cooperate with the authorities, five employees crafted a jokey response saying the robbers had taken KitKat’s “have a break” slogan a little too literally. Nestlé also launched an online stolen KitKat tracker, spinning the bad news into a viral marketing campaign that the company estimates notched $231 million worth of earned media in 10 days—a decent return for a truckload of chocolates worth an estimated $420,000.

“It was about learning to take a risk, be fast and be connected with consumers,” says Navratil. “Speed over perfection, courage over comfort….It’s a good example of the new Nestlé we are trying to build.”

It will take more than stolen KitKats and canny marketing to turn the company around. Shares slumped 43% from December 2021 to January 2025 in a brutal crash that wiped out about $177 billion in market capitalization. That isn’t supposed to happen to Nestlé: Unflashy yet reliable products such as Nescafé instant coffee and Fancy Feast cat food are expected to deliver steady gains and a solid dividend, rather than wild selloffs.

The nightmarish run started when the war in Ukraine forced Nestlé to make adjustments, as key raw materials like fuel and wheat became more expensive. The company responded by raising pricing 8.2% in 2022 and 7.5% in 2023. But by defending margins, it sacrificed market share to rivals such as Oreo and Cadbury owner Mondelez International and soft drinks maker Keurig Dr Pepper.

Shoppers weren’t in the mood to pay more for staples such as coffee, chocolate, and ice cream as inflation squeezed their wallets. The total volume of products Nestlé sold flatlined in 2022 and then slid in 2023.

That wasn’t the only problem. Nestlé tweaked its portfolio, but investors say some acquisitions were a distraction, backfiring as the company expanded into non-core areas.

Nestlé acquired a majority stake in Oakland, Calif.–based Blue Bottle Coffee for $425 million in 2017. Blue Bottle opened about 100 stores and expanded into China and South Korea, but Nestlé still lost money when it exited its position in April for $400 million, according to industry estimates.

It turned out that mass-producing instant coffee gave the company little insight into how to run an artisanal coffee shop. “As a business, it was outside our core competencies,” Navratil says.

The market also questioned the acquisitions of peanut-allergy biotech Aimmune Therapeutics and food-delivery service Freshly. Nestlé divested Aimmune’s signature drug Palforzia in September 2023, about three years after buying the company for $2.6 billion.

Nestlé bought Freshly for $950 million in October 2020. It shut down less than three years later. In May 2023, some Freshly investors alleged that Nestlé failed to pay up to $550 million in earn-outs tied to future growth, a lawsuit Nestlé says is “unjustified.”

The stock fell 31% from January 2022 to August 2024, when the board ousted CEO Mark Schneider, the star boss who had previously helped mastermind shares’ run to a record high.

Schneider was succeeded by Laurent Freixe, who joined Nestlé in 1986 and had been CEO of the company’s Latin America business since 2022. Sales volumes recovered, but Nestlé fired Freixe in September 2025 after the company said an internal investigation found he had an undisclosed romantic relationship with a subordinate. The CEO’s dismissal scuttled any hopes of a quick reset.

Freixe didn’t respond to questions from Barron’s about the company’s

strategy from January 2022 to September 2025. Schneider declined

to comment.

The misery didn’t end there. In January, Nestlé recalled some of its infant formula products after tests found they contained a toxin that can cause vomiting. The company says it is confident in its food safety protocols and acted quickly to fix the problem, which was tied to a quality issue in an ingredient from a supplier.

Nestlé has weathered controversies before, including a U.S. boycott in the late 1970s tied to marketing baby formula as an alternative to breast-feeding in developing countries. The boycott was dropped in 1984 when Nestlé agreed to refine its policy to fit with the World Health Organization’s recommendations.

Cooking Up a Comeback

Navratil and Chief Financial Officer Anna Manz spend a large chunk of their time working on their turnaround plan at Nestlé’s headquarters in Vevey, a small lakeside town where Charlie Chaplin spent the last 25 years of his life.

Manz’s office overlooks Lake Geneva, where a few employees take a lunchtime dip in the summer. After commuting by bus, the CFO often starts her day by tracking which brands and countries are leaders and laggards. The wonders of artificial intelligence mean that what would once have been a weekly bundle of regional managers’ reports is now available as real-time daily sales data.

“People eating and drinking us more is the first step to value share,” the CFO, who joined Nestlé from the London Stock Exchange in March 2024, tells Barron’s.

Just 22 miles away from the head office, the Swiss Alps overlook the Romont coffee plant. Over a shot of Nespresso, Manz lays out some of the things she learned last year, including that Nestlé needs to go all-in on fast-growing global trends like cold coffee and therapeutic pet diets.

The north star for Navratil’s new Nestlé is real internal growth, or what the company calls RIG. The metric measures how volume, rather than prices, is boosting revenue, to assess whether the company is winning market share.

“We want to grow faster than our competitors,” says Navratil, who knows firsthand just how important volumes are. The CEO has worked for Nestlé for about a quarter of a century, with stints in Honduras and Mexico and a spell running Nespresso, a brand sold in 81 countries.

Three-month sales data published in April suggests the strategy is starting to pay off. RIG climbed 1.2% from a year ago, rising across all of Nestlé’s businesses except the troubled infant formula division. Shares jumped 5.9%, their best session since October 2025.

As he boosts RIG, Navratil has set about slimming down Nestlé. The longtime company insider has been acting more like an external hire brought in to shake things up, signaling to investors that he’ll ax billion-dollar businesses if that’s what it takes to change the company’s fortunes.

The new CEO has set out to streamline Nestlé’s portfolio around coffee, snacking, nutrition, and pet care, believing all four segments can deliver high-single-digit revenue growth. Nestlé is exploring selling well-known brands, including sparkling-water company San Pellegrino and the rest of its stake in ice cream maker Häagen-Dazs. Those businesses are lower-growth, harder to scale, and targeted at affluent consumers.

Nestlé isn’t the only consumer goods giant that’s spinning off large parts of its business. Rival Kellogg divided itself in two in 2023, and Unilever has spun off its ice cream business and remaining food assets in recent years. Kraft Heinz has toyed with the idea of a breakup, but suspended plans to split after pressure from major shareholder Berkshire Hathaway.

Adjusting the portfolio isn’t the only area where Navratil has been ruthless. The CEO has moved to cut costs by announcing plans to lay off staff. Nestlé said in October that it would slash 16,000 jobs, or about 6% of its total workforce; it expects its strategic changes to save about 3 billion Swiss francs ($3.8 billion) by 2027.

Still, while it trims the fat in some areas, Nestlé is still filling gaps elsewhere. The company said earlier this month that it agreed to fully acquire ready-to-drink meal maker yfood Labs after a three-year collaboration. It’s the company’s first acquisition under Navratil. Sales for yfood were about 150 million euros in 2025, representing double-digit growth from the year before.

The company is also going all-in on AI, with factory workers in the process of digitalizing paper records.

These early moves have reassured investors, with the stock up about 4% since Navratil replaced Freixe. But Nestlé must address three other challenges to lift its bruised shares.

First, Navratil and Manz need to get better at showing investors how they plan to address the challenge posed by GLP-1 weight-loss drugs, which have led to some consumers losing their appetite for snacks.

“We sell nutrition, not calories….People will still have the occasional piece of chocolate or pizza,” Navratil tells Barron’s. To some, that doesn’t inspire confidence that Nestlé has a grand plan to maintain strong sales of Hot Pockets and Toll House baking chocolate in the age of Ozempic.

The war in Iran is another worry. Economists expect a surge in inflation if shipping through the Strait of Hormuz remains disrupted, which would once again put Nestlé in a tough position of choosing between hiking prices and growing volumes.

Lastly, investors need more clarity about Nestlé’s intentions around its stake in cosmetics giant L’Oréal. It has held a position in the Garnier and Maybelline owner since 1974, when it bought in at the request of L’Oréal heiress Liliane Bettencourt to help stop the French government from nationalizing the company. It currently holds about 20% of all shares, a position valued at just under $47 billion. Nestlé bought the stake for just CHF300 million ($382 million) in 1974. It structured a sale in 2021 as a buyback, whereby L’Oréal purchased and then canceled shares, meaning Nestlé didn’t have to pay capital-gains tax on the transaction.

Asked why Nestlé is resistant to selling its L’Oréal shares, which are roughly flat over the past year, Manz tells Barron’s it has been “a very high-performing investment” for the company. “What will really drive our share price going forward is brilliant execution, and anything outside of that is a distraction, frankly,” she adds.

L’Oréal stock fetches about 28 times expected earnings for 2026, a premium to Nestlé. Investors say that if the company believes its turnaround plan has legs, it should sell the stake and buy its own shares or pay down some of its net debt pile, which stood at CHF51.4 billion at the end of 2025.

“There’s a wide valuation gap between the two companies, and Nestlé using that capital to buy back shares would be the right thing to do,” says Barron’s Roundtable panelist Christopher Rossbach, chief investment officer of the private investment partnership J. Stern, which holds a position worth $54 million in Nestlé. “Now would be the time to sell some of it, if not all of it.”

A Sweet Spot

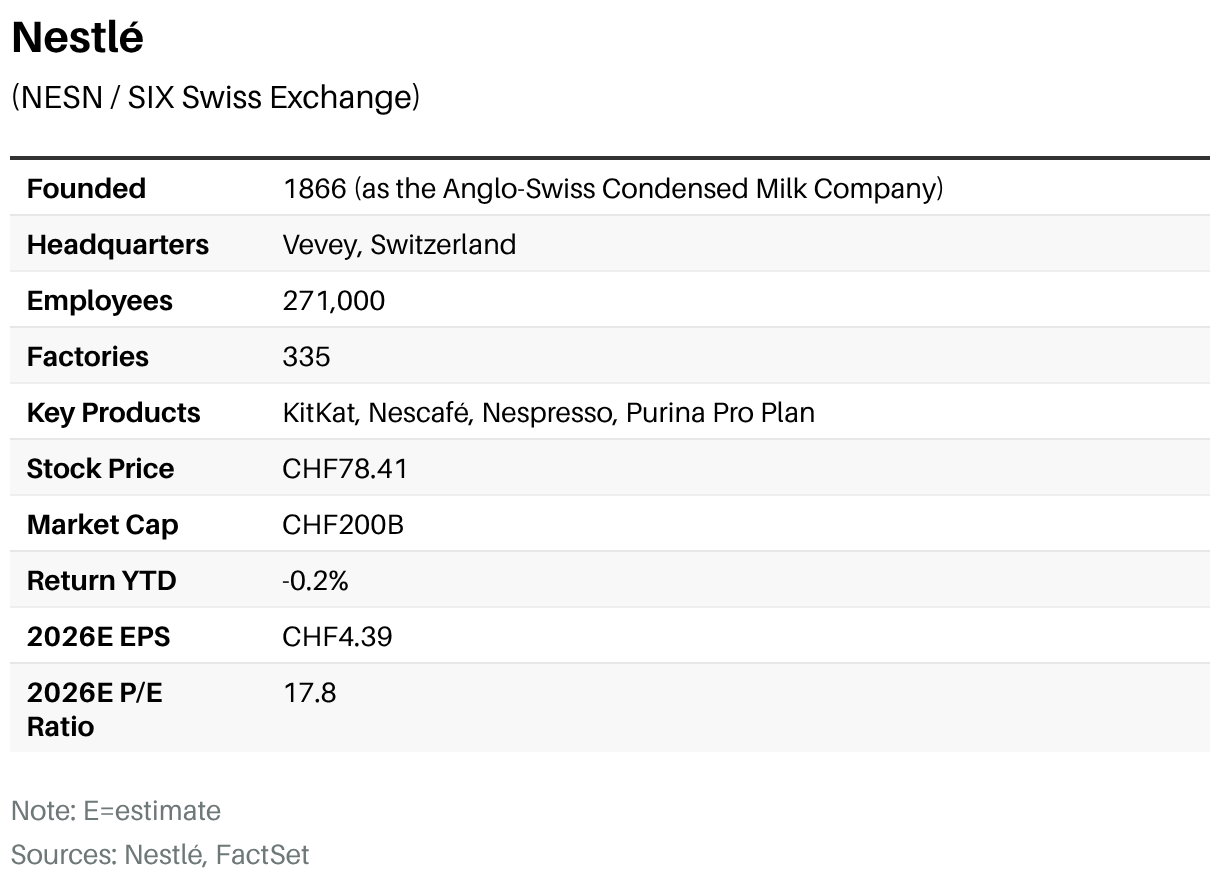

If Nestlé clears those hurdles, there is plenty for investors to like. Shares are trading at about 18 times forward earnings, a sizable discount to the 23-times valuation they’ve had on average over the past five years. That is cheap for a company expected by analysts to increase its underlying trading operating profit by 21% from last year to 2030.

Wall Street is forecasting annual free cash flow will rise to CHF12.9 billion from CHF9.2 billion by then. That bodes well for a dividend that has risen every year since 1996. Nestlé paid out CHF3.10 a share last year for a yield of 3.94%.

There’s a broader buy case, too. Shares in consumer goods makers have been depressed ever since the pandemic, but they could rally as investors seek to shield their portfolios from a potential AI bubble by loading up on stocks that can deliver reliable returns, year after year.

There are signs that a rotation away from highflying tech stocks may be coming, with the Nasdaq Composite slumping 4% on June 5 as investors slammed the brakes on the AI trade.

Brian Kersmanc, a portfolio manager at GQG who oversees a $1.8 billion stake in Nestlé, thinks the consumer staples industry is in a “digestion phase,” where shoppers are still adjusting to the price hikes that came about during and immediately after the pandemic. He expects Nestlé’s revenue growth to reaccelerate as it optimizes its portfolio around areas like coffee and pet care. “A lot of these types of businesses will catch a bid as people rotate out of tech and try to find something else that can deliver high-single digit or low-double digit returns,” he tells Barron’s.

Nestlé’s suite of reliable and steady products can help it ease investors’ AI jitters and serve as a hedge against volatile tech stocks. What matters above all is achieving consistent growth. The company is targeting organic growth of 3% to 4% this year, which some on Wall Street see as a tough ask.

“We need to come back to this consistent delivery,” Navratil tells Barron’s. “All of this has started and is under way, but we’re far from done.”

If he’s right, the innovative handling of the KitKat heist won’t be the only sign that the turnaround plan is working. Just like the missing 413,793 chocolate bars, Nestlé stock will be a steal.

Write to George Glover at george.glover@dowjones.com