Regulators, lawmakers, and consumer groups are fighting over what it means to be a community bank. The debate has implications for lenders and borrowers everywhere.

The Walton State Bank has served 200-person Walton, Kan., since 1907, when the state granted Guy Hawk a charter to start a local bank. Some 45 original stockholders invested alongside Hawk, a sewing machine salesman.

Today, the bank’s lone branch sits on Walton’s Main Street and has $12.5 million in assets. It specializes in loans for purchasing farmland and cattle. It’s a community bank, in spirit and statute: a small asset base, local client relationships, and straightforward financial services.

Origin Bank, based in northern Louisiana, has also been considered a community bank since its founding in 1912. With 60 locations in five states today, it bears little resemblance to Walton. Origin drew scrutiny this past fall after disclosing loans it made to the bankrupt subprime auto lender Tricolor Holdings, whose CEO sat on Origin’s board and saddled a web of banks with losses.

As community banks, Origin and Walton are subject to less rigorous monitoring and oversight than their largest counterparts like JPMorgan Chase and Bank of America, or big regional lenders like Citizens Financial Group and Zions Bancorp. The Federal Reserve’s definition of community bank—those with up to $10 billion of assets—covers roughly 96% of America’s federally insured lenders.

Industry groups and key regulators now say that isn’t broad enough. In fact, the definition of community is turning into one of the primary financial regulatory debates of President Donald Trump’s second term.

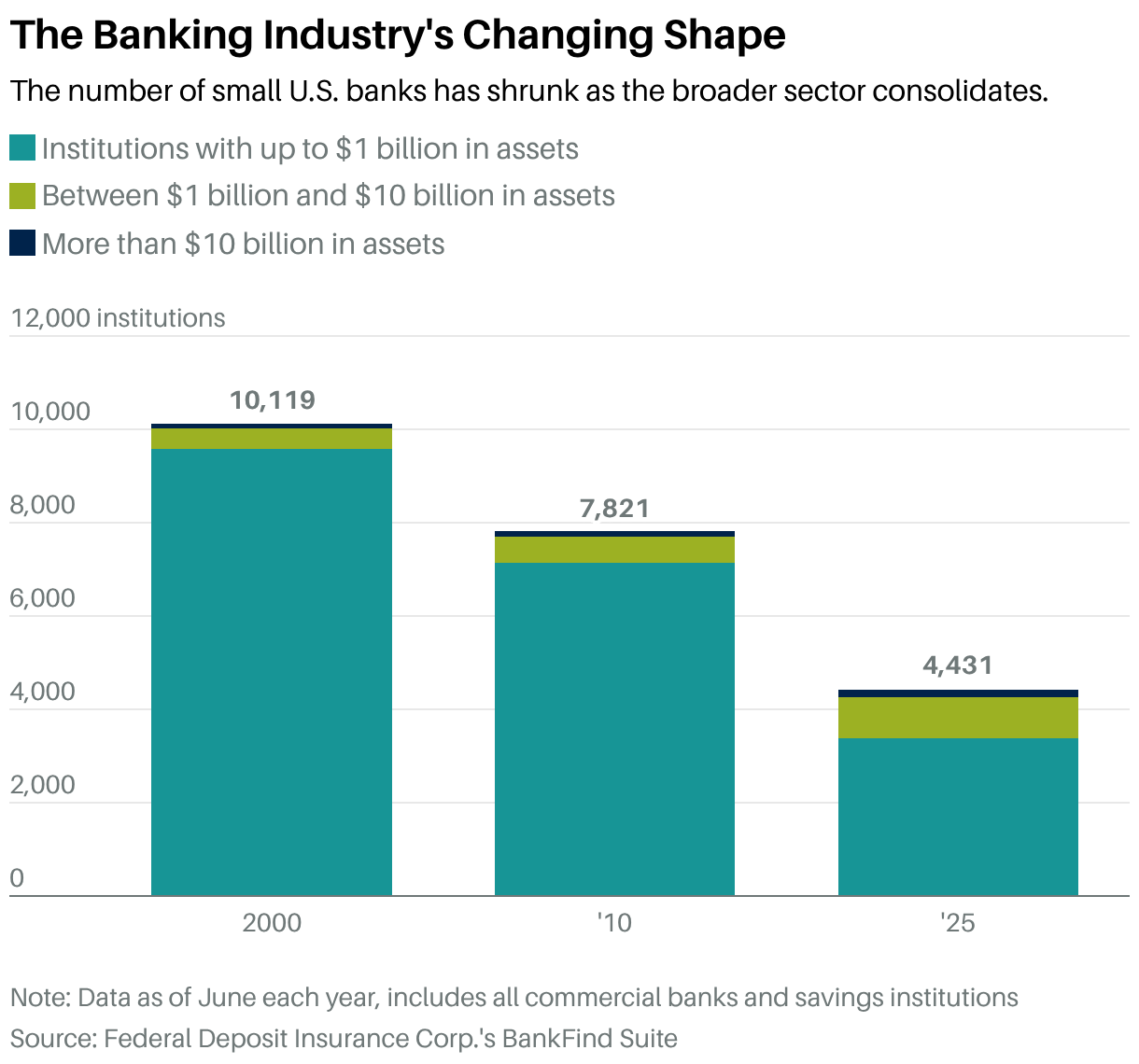

In recent months, the Office of the Comptroller of the Currency, or OCC, and the Federal Deposit Insurance Corp. have raised the threshold for community banks to $30 billion when it comes to essential regulatory functions like merger applications and regulatory exams. Under a $30 billion framework, all but 70 or so of the nation’s 4,276 lenders would be considered community banks.

That’s a necessary corrective, according to some Republicans. “Dodd-Frank sought to end ‘too big to fail,’ but in fact, it created a regulatory environment in which community banks are ‘too small to succeed,’ ” said Sen. Bill Hagerty (R., Tenn.) during a Senate Banking Committee hearing in February. “For smaller banks, the result has been a bloodbath. The U.S. has lost 3,600 community banks since 2010.”

Community groups and some Democrats say that relaxing community definitions could have unintended consequences, including losing the benefits of community-focused lending.

“Community banks play a critical role in supporting local economic growth through relationship-based lending, local decision-making, and a strong commitment to the communities they serve,” says Rebeca Romero Rainey, CEO of the Independent Community Bankers of America, or ICBA. “That’s what defines community banking—a focus on accountability, local engagement, and meeting the needs of customers.”

The National Community Reinvestment Coalition, or NCRC, an economic-justice advocacy group that negotiates community-benefits agreements between banks and community groups, says the OCC’s plan undermines the 1977 Community Reinvestment Act, which requires banks to serve their local communities, including low- and moderate-income neighborhoods.

“If agencies conduct cursory reviews of these applications, they are likely to fail in their requirements to ensure that banks confer public benefits,” wrote Jesse Van Tol, CEO of the NCRC, in a letter to the OCC in January.

The rule went into effect in April.

Under the $30 billion cap, more consumers are likely to bank with firms whose loan book quality is less scrutinized than it once was, for instance, or that are required to hold less capital on their balance sheets.

“I think it is fair to say that $30 billion banks aren’t really ‘community banks’—at least a lot of them could be multistate, complex operations,” says David Zaring, a professor of legal studies and business ethics at the Wharton School of the University of Pennsylvania.

Larger banks, meanwhile, could face competition from smaller banks if they can afford to allocate money away from regulatory compliance costs and toward more services.

The debate playing out over the definition of community is part of the government’s most significant bank-regulation overhaul since the 2008-09 financial crisis. Democrats including Sen. Elizabeth Warren of Massachusetts and Rep. Maxine Waters of California are pushing back on regulators’ efforts, saying that Trump-appointed officials are angling for less oversight under the cover of helping local communities.

“Policies are disfavoring the safest institutions that provide the most support to the Main Street economy—community banks—by massively and unfairly favoring the riskiest institutions—big banks, crypto banks, and fintech firms,” said Phillip Basil, director of economic growth and financial stability at Better Markets and a former financial institution policy specialist at the Fed.

Truist Securities analyst Brian Foran says the term “community banking” has lost some meaning in the digital banking era. Consider financial-technology firm Chime, which offers banking products through two lenders that fit the regulatory definition of community banks, each with under $10 billion of assets. Chime opened 13% of all checking accounts in the U.S. last year, Foran noted. “That is a big community!”

The NCRC calls out the need for local branches even in a digital world. “The presence of branches is critical for traditionally underserved communities, so they are not forced to rely upon expensive payday lenders or check cashers,” the group wrote in its recent letter. Such branches could get less attention under new community standards, it added.

Bank lobbies recognize that their position in Washington, D.C., may never be stronger and are pushing for as much change as possible before the next wave of elections.

Still, there are limits to what regulators can pass on their own. The Fed probably wouldn’t raise its $10 billion limit in part because it would require an act of Congress, says Raymond James analyst Daniel Tamayo. It can, however, adjust how it oversees small to midsize banks through rule-tailoring without congressional approval, Tamayo says, “and we think this is increasingly likely.”

He says the move could save banks several million dollars a year in compliance costs as they cross the $10 billion asset threshold.

At the Fed, bank lobbyists pushing for lighter small-bank regulation have won an influential ally: Vice Chair for Supervision Michelle Bowman, the Fed’s top bank regulator, for whom community banking is personal.

Her family has been in the business since 1882, when her great-great-grandfather helped form Farmers & Drovers Bank in Kansas. She worked there from 2010 to 2017.

“My most challenging role was as compliance officer—working with our small team to implement many of the new postcrisis regulations,” she said in 2018. “Although the crisis revealed weaknesses in the U.S. financial system that needed to be addressed, I have witnessed firsthand how the regulatory environment created in the aftermath of the crisis has disadvantaged community banks.”

Bowman favors increasing “static and outdated” asset thresholds on small lenders.

Meanwhile, community banks are aiming to protect their domain. In a new advertising campaign, the Independent Community Bankers of America attacks credit unions for undermining their mission while avoiding federal taxes. “Big credit unions have perfected their act: While presenting themselves as community champions, they quietly make accountability, tax fairness, and consumer choice disappear.”

In response, the credit unions accused the ICBA of hypocrisy and touted their own community status.

“Let’s be honest about what this really is,” Jason Stverak, chief advocacy officer with the Defense Credit Union Council, said at the time, “a well-funded attempt by the banking lobby to distract policymakers from its own preferential tax treatment while attacking the cooperative financial institutions that millions of Americans trust.”

Write to Rebecca Ungarino at rebecca.ungarino@barrons.com