The prospect of billions of dollars of oncoming demand for SpaceX stock from index-tracking funds risks creating a feedback loop that drives the shares of Elon Musk’s company even higher, academics and market observers have warned.

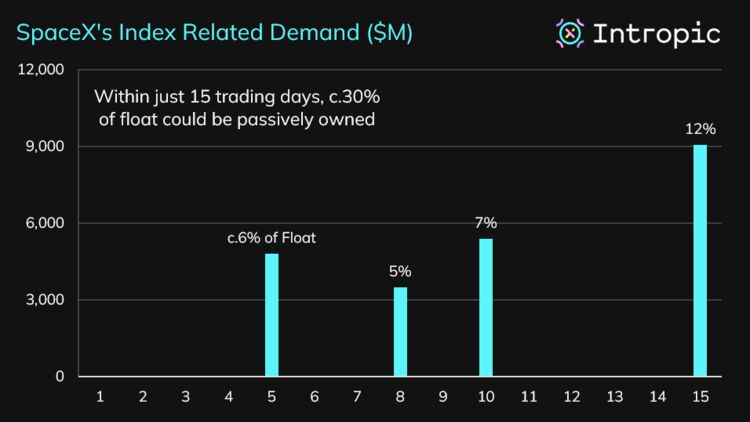

Nasdaq Inc., FTSE Russell and MSCI Inc. are all set to fast-track the company into their gauges, after the first two index providers changed rules to allow its early addition. About 30% of SpaceX’s free float is now set to be owned by passive investors after just 15 days of trading, according to Intropic, a provider of index-rebalancing forecasts. That figure would be roughly 4% under previous slower-inclusion rules.

Anticipation of that mechanical demand alone is set to put upward pressure on SpaceX stock, even before the race between funds to secure shares. Combined with the frenzies already surrounding Musk, SpaceX and artificial intelligence, the risk is that index products themselves help drive up the price they end up having to pay.

It makes the rocket maker’s public debut not only the largest in history, but also a significant test of passive investing’s influence on the market.

“One reason every index provider is trying to add SpaceX to their index so fast is because of the implicit competition between benchmarks,” said Marco Sammon, an assistant professor at Harvard Business School, who has studied the impact of passive investing. “This seems like a case where index methodology, rather than fundamentals, could have a huge effect on prices.”

‘Shadow Tax’

With passive vehicles now accounting for about 60% of US equity funds and controlling about a fifth of the S&P 500’s value, according to Bloomberg Intelligence estimates, concerns have long been growing that indexing has the potential to warp trading and prices.

Sammon at Harvard has previously shown that widespread anticipation of index additions has actually helped contain any upward pressure they exert on price, thanks to specialized traders at hedge funds and market makers acquiring shares gradually ahead of time. These intermediaries are then ready to offload holdings when index funds need them, he showed in a working paper with John Shim and Stefano Pegoraro at the University of Notre Dame.

The problem: fast-tracking new stocks leaves arbitrageurs with less time to build up inventory, Sammon said.

Read more: SpaceX IPO Forces Wall Street to Reorganize Around It

In separate research , he and Harvard colleague Chris Murray looked at CRSP, an index provider with a mechanism to fast-track some IPOs. They found companies added early outperform by five percentage points leading up to the index addition date, with the effect reverting within three weeks. The fast-tracked names also raise more capital in their offerings — a sign rigid passive demand has real economic consequences.

It effectively amounts to a “shadow tax” on passive investors who have to buy high and also the company, which can’t sell directly to index trackers.

“When the window is compressed, the same amount of mechanical demand is more likely to generate relatively more temporary price impact and subsequent reversal,” said Sammon. “This is compounded by the post-IPO market being generally volatile and illiquid. In such cases, the cost for index fund investors will be larger.”

Reflexive Loop

For index providers, the decision to fast-track a company is a call between potentially rushing into an over-hyped name or missing out on an industry giant making its public debut. As well as SpaceX, major offerings are expected soon from both OpenAI and Anthropic.

S&P Dow Jones Indices, which compiles the all-important S&P 500, has rejected proposals that might have seen all three names enter America’s benchmark gauge early.

Companies are now going public at a more mature stage and fast-tracking IPOs is “helping indexes better represent all the public companies that matter to the economy,” Nasdaq economists Phil Mackintosh and Nicole Torskiy wrote on the firm’s blog last week. Stocks that enter the Russell 1000 first have tended to beat the S&P 1500, they wrote based on 2010 to 2025 data.

Even so, the expected passive demand for SpaceX stock could create a “reflexive loop,” Intropic said. Flows will be determined by the company’s market value on the rank date for each index, it wrote in a Monday blog post, and that could be temporarily inflated by arbitrageurs building up a position to prepare for the mechanical bid.

The loop may even extend to the IPO price, if investors participating in the offering are doing so in anticipation of passive demand, Intropic said.

“The price impact of passive flows is short-lived, but it could disrupt price discovery at arguably the most important point of a company’s stock market journey,” the London-based firm wrote.