Ever since Italian finance descended into a deals frenzy almost two years ago, Carlo Messina remained on the sidelines. Intesa Sanpaolo SpA would not be part of it, its chief executive officer repeatedly said.

On Monday, Messina demonstrated he was just biding his time as Italy’s largest bank unveiled a €30.6 billion ($35.3 billion) offer for Banca Monte dei Paschi di Siena SpA in what would be Europe’s biggest bank takeover in almost two decades. Overnight, the 64-year-old went from an ostensibly passive spectator to the biggest driver of Italian bank consolidation, vowing to see the deal through.

“If someone is prepared to offer more than we are offering, then there could be competition,” Messina said in a Bloomberg TV interview Tuesday. In an indication of the scope of his ambition, he said that targets elsewhere in Europe could be next on his shopping list.

To pull the deal off, he will have to overcome stiff competition. Banco BPM SpA has already made a rival pitch to Monte Paschi and Intesa’s biggest domestic rival, UniCredit SpA, is likely considering its options too. CEO Andrea Orcel previously tried to buy Banco BPM and has said he continues to be open to deal options in his home market.

Messina’s move is “classic alpha-player behavior: when you already sit on the throne, you don’t tolerate new pretenders at your back,” said Carlo Alberto Carnevale Maffe, a professor of business strategy at Milan’s Bocconi University. “Despite months of solemn denials, the moment there was a risk to his dominance, even the most disciplined of Italian bankers turned predator.”

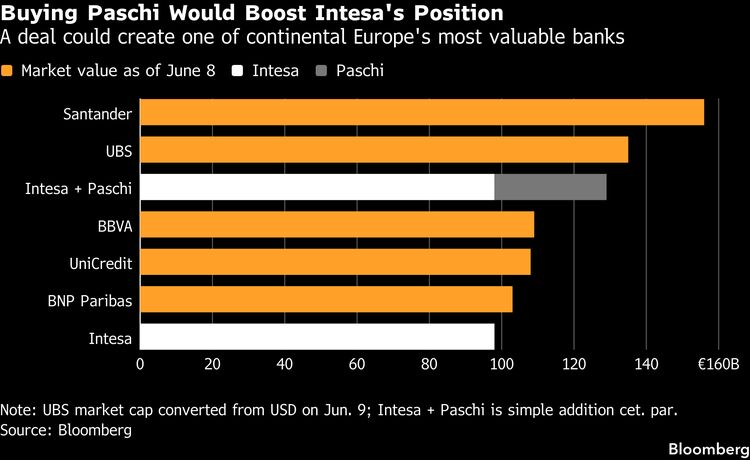

If Messina ends up buying Monte Paschi, it will make Intesa’s lead on UniCredit in Italy even more difficult to close and cement its position as the country’s biggest lender by far.

The deal would add 635 branches to Intesa’s existing roughly 2,600. The lender’s acquisition of Mediobanca SpA last year would also hand Messina substantial wealth management and investment banking operations.

Monte Paschi said in a statement Monday it’s assessing the proposals from Intesa and Banco BPM.

Intesa’s strong position in Italy was what previously prevented Messina from getting involved in domestic deals as it may have created competition issues, Messina said in the interview. The breakthrough was delivered by a parallel transaction he had been stealthily negotiating since January with insurer Unipol Assicurazioni SpA to offload large chunks of Monte Paschi’s branch network and its brand.

Unipol has agreed to pay as much as €3.5 billion for the assets and it plans to subsequently merge the acquired assets into BPER Banca SpA, in which it’s the largest shareholder. The move would substantially boost BPER’s size.

Messina’s play isn’t only about Monte Paschi. The lender owns a 13% stake in Assicurazioni Generali SpA, the country’s largest insurance firm that has attracted intense deal interest in the past. Messina himself tried to buy Generali a little less than a decade ago.

Monte Paschi’s Generali stake, acquired as part of the Mediobanca takeover, has long been a prized asset in Italian finance because of the insurer’s earnings contribution and the influence it brings in the sector. It was partially why two of the largest investors in both Monte Paschi and Generali — construction tycoon Francesco Gaetano Caltagirone and the Del Vecchio clan’s holding company Delfin Sarl — backed the Mediobanca deal last year.

Messina said Generali isn’t a priority in the offer and ruled out a full-blown acquisition. He also said he expects his offer will get support from Caltagirone and Delfin.

Intesa’s bid for Monte Paschi creates a situation like “Game of Thrones in Italy,” Morningstar DBRS Arnaud Journois said in a note. The move “should accelerate consolidation in Italy.”

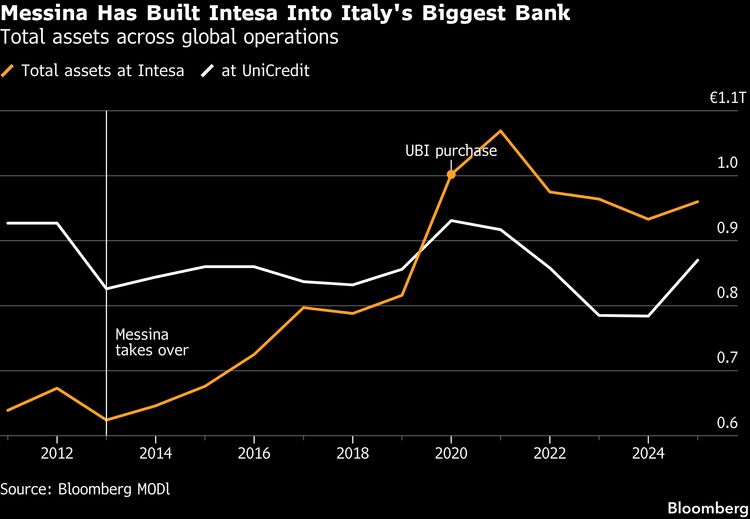

Messina joined what was then Banca Intesa SpA in the 1990s, rising through the ranks to become chief executive officer in 2013. Banca Intesa bought rival Sanpaolo IM SpA in 2006, creating Intesa Sanpaolo.

While Messina has stayed away from big acquisitions more recently, he’s pulled off several major transactions since assuming his role. In 2017, he bought assets from two failed regional lenders, Veneto Banca and Banca Popolare di Vicenza, and in 2020 he acquired UBI Banca. The firm after exploring a deal for Generali decided to abandon its effort in 2017.

The deal involving the regional banks was a particular coup as Intesa ended up paying €1 for the parts of the two banks that were still considered healthy. The Italian government added €5.2 billion to help maintain the targets’ capital ratios, further sweetening the deal for Messina.

Boosted by higher interest rates, Intesa’s profitability has soared in recent times, with net income hitting a record €9.3 billion last year. Messina in February vowed to pay out €50 billion to investors over five years, though he also said at the time that he wasn’t planning to do any domestic deals.

| Read more about Intesa’s past deals |

|---|

| Intesa and Sanpaolo Boards Back EU32.6 Billion Offer (2006) |

| Intesa Rises After Giving Up Generali Merger Plan (2017) |

| Intesa CEO Wins Big From Collapse of Two Veneto Banks (2017) |

| Intesa’s UBI Deal May Stir Dormant Italian Banking M&A (2020) |

The proposed acquisition of Monte Paschi would be the largest transaction yet in a consolidation wave that started engulfing Italian finance from late 2024. Banco BPM has since acquired asset manager Anima Holding SpA and Monte Paschi bought Mediobanca. A takeover bid by UniCredit for Banco BPM was unsuccessful.

The government in Rome played a crucial role in the aborted UniCredit offer for Banco BPM as well as the abandoned effort of Generali and French bank BPCE to combine their asset management operations. The administration under Prime Minister Giorgia Meloni has long advocated for a third big lender to rival Intesa and UniCredit and it’s been protective of assets it sees as strategic such as Generali.

The Italian government said in a statement Monday that it was informed of Intesa’s plan and that the offer reflects the value of the bank. It stopped short of taking sides in favor of either Intesa or Banco BPM, stressing that the offered price is what matters most.

For Messina, the deal wouldn’t just be a crowning career achievement. He said in the interview it would pave the way for him to step up his ambitions even further and start chasing deals outside Italy.

The acquisition of Monte Paschi would be just “a starting point,” he said, adding he would then start to “look at the consolidation in Europe in a position of total strength.”