When Banca Monte dei Paschi di Siena SpA sealed its hostile takeover of Mediobanca SpA last year, the financial rationale was dubious but the politics were clear: Italy wanted a third major lender to compete with its top two. Now, one of those leading banks, Intesa Sanpaolo SpA, has launched a €30.6 billion ($35.3 billion) bid for the enlarged Monte Paschi and the picture is reversed: For investors, the strategy mostly adds up, but the politics make almost no sense at all.

As ever with Italian banking, things aren’t totally straightforward. But I’m skeptical that either the government or Monte Paschi’s powerful significant minority shareholders, especially the billionaire Francesco Gaetano Caltagirone, will back Intesa.

Monte Paschi had been widely expected to strengthen its status as Italy’s third major bank by pursuing a combination with Banco BPM SpA — indeed, BPM rushed out its own merger-of-equals proposal on Sunday. Plus, a major factor in Monte Paschi winning its fight for Mediobanca was Caltagirone’s determination to gain indirect control of the latter’s 13% stake in insurer Generali Spa. An Intesa takeover frustrates both these efforts.

To take a step back, Italy has been going through a much-needed consolidation in financial services, but one beset by political interference. Partly that was down to the government’s previously large stake in Monte Paschi, acquired through a series of bailouts of Italy’s long-term financial basket case. Under Prime Minister Giorgia Meloni, it finally found a solution to support when the much-restored Monte Paschi moved for Mediobanca. The government got to offload the last of its stake as part of the deal and Italy got a more competitive banking market with a third big player.

But the political meddling has also been driven by a misplaced protectionist agenda. The government in effect blocked UniCredit SpA’s bid for Banco BPM by invoking powers linked to national security. Its opposition also scuppered a tie-up between the asset management arm of Generali and Natixis SA of France. There were murky motivations behind both interventions.

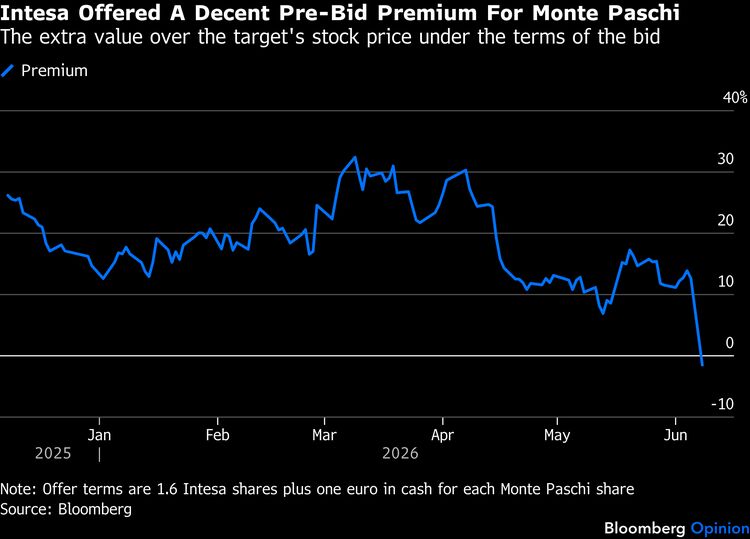

All of this matters for Intesa’s offer – and most of it should count against the bidder.

First, there’s the proposal itself. Intesa is offering 1.6 of its own shares plus €1 for each Monte Paschi share. That makes for a 17.4% premium to the target’s volume-weighted average price over the past three months, and 10% compared with Friday’s close. This isn’t bad considering Monte Paschi’s stock price had rallied more than 20% in the three months through the end of last week.

Intesa’s rationale is to beef up in investment banking, wealth management and some Italian operations. “ We aim to be the Italian UBS,” Chief Executive Officer Carlo Messina told investors on a call Monday, referring to Switzerland’s biggest bank, UBS Group AG.

To head off potential antitrust concerns within Italy, Intesa has an agreement to sell the Monte Paschi brand, 635 of its branches, its headquarters and parts of its business that contribute about 20% of its net income to the insurer Unipol Assicurazioni SpA. That will also give Intesa as much as €3.5 billion of cash to help fund the takeover.

Unipol could become an alternative foundation for the government’s desired third pillar of Italian banking instead of the acquired Monte Paschi if it pursued a deal with another mid-sized lender, such as BPER Banca SpA, but this is speculative at best.

Messina offered another political sweetener by claiming there would be no involuntary job cuts under his deal. More than that, Messina said the bank’s existing plan to make 6,800 new hires would go ahead on top of a similar number that would join in the takeover. Combined, he called this “ one of the most ambitious hiring programs ever seen in our country, focused on young people in Italy.” Its experience with integrating businesses meant a risk-free merger and would deliver €1.5 billion of cost savings, he claimed. Investors should note these savings replace rather than add to the reductions that Monte Paschi hopes to get out of Mediobanca. Regardless, I would take all of this with a pinch of salt – especially the promises on jobs.

Messina also thinks he has an appeal to Italy’s protectionist tendencies. Banco BPM has a big French shareholder in Credit Agricole SA, which holds just over 20%. If the government objected to UniCredit buying BPM, it should also oppose BPM merging with Monte Paschi, he argued. Well, maybe, although that combination would dilute the French influence significantly, so maybe not.

There’s another dilution that could count against Messina — that affecting Caltagirone and the family trust of the late Leonardo Del Vecchio, which currently own 10.3% and 17.5%, respectively, of Monte Paschi. The deal would minimize their ability to influence what happens at Generali through Monte Paschi’s stake in the insurer, which Intesa would keep. Messina said he had good relations with these two investors and suggested they would have a positive view of his proposal. That has yet to be seen.

Monte Paschi shares jumped nearly 13% on Monday, more than erasing the Intesa offer premium at Friday’s close. Its investors might be hoping they’ll get to enjoy a bidding war for their bank. I’m not convinced they will.

More from Bloomberg Opinion:

-

Hong Kong's Private Wealth Bankers Should Be Anxious : Shuli Ren

-

Bankers Flocked to Paris. It Still Can't Gloat : Lionel Laurent

-

Monte Paschi Coup Only Hurts Its Backers : Paul J. Davies

Want more from Bloomberg Opinion? OPIN <GO> . Or subscribe to our daily newsletter .