This is an interactive article, which is supposed to be read in a browser.

Name: Anonymous

Submitted date: March 16, 2026

I know multiple people who have lost their livelihoods because a bank decided that what they provided was ‘obscene.’

Name: Anonymous

Submitted date: March 12, 2026

My bank shouldn’t be able to see me buy porn and immediately think I am unfit to have a bank account.

Name: Anonymous

Submitted date: March 15, 2026

Regardless of whether you’re buying recreational marijuana or guns or MAGA hats, the ability to make that purchase should not sit in the hands of some wealthy bank board members.

Policy wonks are often the main turnouts when the Federal Reserve seeks public comment on a new rule for banks. But recently, hundreds of pornography enthusiasts stepped forward, too.

So did gun lovers, members of the LGBTQ community, gamers, furries, artists, librarians, libertarians and at least a couple of White supremacists. On one issue, they almost all agree.

They’re supporting a proposed Fed rule change inspired by Donald Trump’s bashing of “ debanking .” The president, who was kicked out of several banks after his supporters stormed the Capitol on Jan. 6, 2021, is demanding that US regulators stop encouraging financial firms to cut ties with customers whose pursuits are legal but might pose a “reputation risk.”

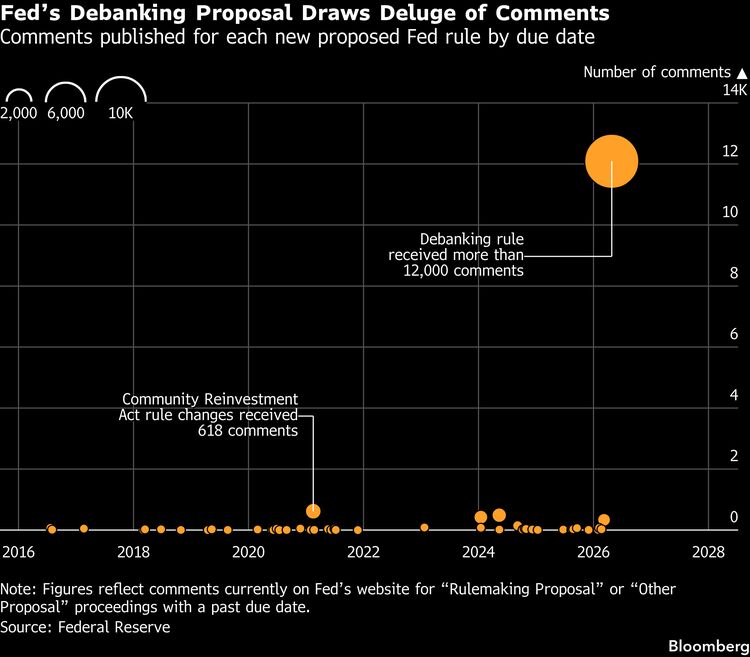

The Fed’s proposal to do just that has ignited a burst of public involvement rarely if ever seen in its modern rulemaking. Its draft regulations typically attract a few dozen comments, or occasionally hundreds. Tally up every letter currently on the Fed’s website about other matters over the past decade and the total is less than 3,500.

But then came the anti-debanking measure, which has drawn more than 12,000 responses so far. It began with a flood of letters in March, continued through April and kept trickling in through May, even as the Fed’s deadline passed. Almost all of the commenters expressed opinions supporting the proposal (a Bloomberg review identified only a few dozen clearly opposed).

Its passage would lift a burden for banks, whose leaders have bristled at regulatory pressure to scrutinize and reject customers. Letters suggest many banks and other platforms have made a mess of it.

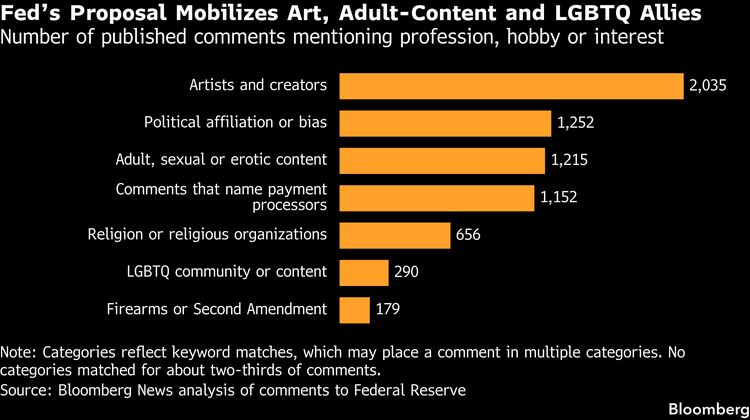

Commenters describe losing access to financial services after engaging in legal activities, while others expressed fear of being targeted for exercising free speech or pursuing the arts. Among people who specified a type of expression, more than 1,200 mentioned pornography or erotic drawings, literature and games.

The result is that the Fed’s staid website now features letters from throngs of people describing sexual desires, fetishes and other sensitive interests, such as a fan of “risqué pinup-style” drawings complaining about how financial firms keep stymying his attempts to commission art from Japan. Other writers span a variety of subcultures, including furries seeking access to erotic animal costumes or cartoon drawings (as one explained, “like those in Zootopia 2 ”).

Overall, more people stepped forward to champion access to adult content than the 618 commenters who weighed in a few years back when the Fed revamped oversight of the Community Reinvestment Act. That landmark law helps people in low-income neighborhoods get home loans and other financial services.

But the stakes are high for debanking, too. Some artists and entrepreneurs described how they or acquaintances struggled to make rent or buy food after financial firms rejected them directly or threatened the online marketplaces where they sell goods.

Vocal constituencies also include people reporting a crackdown on LGBTQ culture or worrying about access to firearms. Comments on religion were split between protecting it from suppression or blaming it for debanking.

“It feels to me like a larger moral panic, and this is just one avenue through which it’s being enforced,” San Francisco Bay Area resident Alexandra Theodotou said in an interview about her decision to write to the Fed. So many people are taking issue with the system because they realize reputation risk is “so vague that it can be used for whatever is politically convenient or financially convenient.”

The Fed’s anti-debanking proposal, known as R-1884 , is simple. In effect, it would tell the regulator’s examiners to stop scrutinizing whether banks have set up systems to spot clients who might create scandals, alarm other depositors and hurt stability. As the Fed put it, staffers would no longer press banks to eject “politically disfavored but lawful business activities perceived to present reputation risk.”

Name: Anonymous

Submitted date: March 12, 2026

As an artist this has made expressing myself SIGNIFICANTLY harder. My freedom of expression is being choked.

Name: Anonymous

Submitted date: March 11, 2026

The debanking of queer or targeted individuals is a life-destroying and heinous act of hatred which should not be tolerated.

Name: Chloe Kaczvinsky

Submitted date: March 30, 2026

We have seen a series of social media platforms, games and other storefronts, and various content creators be forced to remove all content deemed ‘immoral.’

Name: Tyler Mene

Submitted date: March 22, 2026

It’s very stressful knowing that one day the morality of the bank I use may arbitrarily change in a way that deems my work no longer appropriate.

Name: Anonymous

Submitted date: March 12, 2026

Who are you guys to tell me if I can buy furry porn or not? You’re not my mom and even my mom doesn’t care.

One of the relatively few opponents of that rollback is US Senator Elizabeth Warren. She and others argue that the longstanding rules, when followed correctly, were supposed to spur banks to weed out customers like Jeffrey Epstein.

Under the Fed’s proposal, examiners inside banks would not “be able to even ask about the extent of their ties to Epstein,” Warren and fellow Democratic Senators Jack Reed and Chris Van Hollen wrote in a joint letter. “As a result, banks may be inclined to overlook clients showing indicia of fraud or other illegality so long as the relationship proves lucrative.”

In Epstein’s case, firms such as JPMorgan Chase & Co., Deutsche Bank AG and Bank of America Corp. handled money for him or his associates for years after he pleaded guilty to procuring a minor for prostitution. The banks later agreed to pay more than $500 million to settle claims their financial services helped enable his sex-trafficking. The firms either disputed or didn’t admit to the allegations, saying afterward that they wanted to help survivors or support anti-trafficking efforts.

Carefully removing such problematic clients can be labor intensive. Firms have tried to make the process more efficient — even automating some scrutiny — to keep costs in check, only to face public backlash from people insisting they got cut off without doing anything wrong.

Many commenters to the Fed said they can easily find graphic content in mainstream media, with at least a dozen people noting that they can watch scenes of incest in Game of Thrones . Yet, they said, financial firms may block them from paying an independent performer, artist or writer for similar content. That effectively puts banks in charge of the creative arts.

“I have seen the specter of reputation risk used by payment processors to unfairly target COMPLETELY LEGAL content being created by small-scale artists over and over again,” wrote one commenter, Scarlett O’Hairdye, whose social media posts inspired others to comment, too. “This is primarily adult content, but safe-for-work queer content has also been caught up in the purges.”

That’s what happened to Texas author Melissa Eaden, who in an interview described her genre as adult queer urban fantasy monster romance. A series she wrote about two men navigating love while one turns into a mythical beast scored high marks on Goodreads. After an Australian group that campaigns against the harmful effects of pornography called on financial firms to disconnect the marketplace Itch.io because of graphic video games, the platform made swaths of mature content unsearchable, throttling Eaden’s sales there. She felt targeted.

“They can’t sue me for what I’m writing so they’re going to take the means for me to actually make a living,” she said.

Eaden noted that both sides of the political spectrum are discovering that power: Despite protections against government censorship under the First Amendment, they can get the other debanked.

Both sides are also realizing they can be debanked. The Christian Employers Alliance, representing “faith driven” businesses and organizations, wrote in a comment letter that its beliefs and “moral conviction” may be labeled as too controversial or considered high risk. It said firms should stick to financial criteria, not ideology.

Likewise, banks shouldn’t be allowed to thwart gun sales, eroding the right to bear arms, Mississippi Treasurer David McRae wrote in a comment letter. “Access to our financial system and the ability to freely express our constitutional rights should never hinge on the political preferences of Wall Street,” he said.

Clues to what drove the deluge of comments are scattered across social media. In early March, an erotic art advocacy group alerted people on Bluesky that the Fed was seeking input on debanking. When other people added instructions on how to weigh in, niche message boards including on gamer and tech websites amplified the posts or made their own.

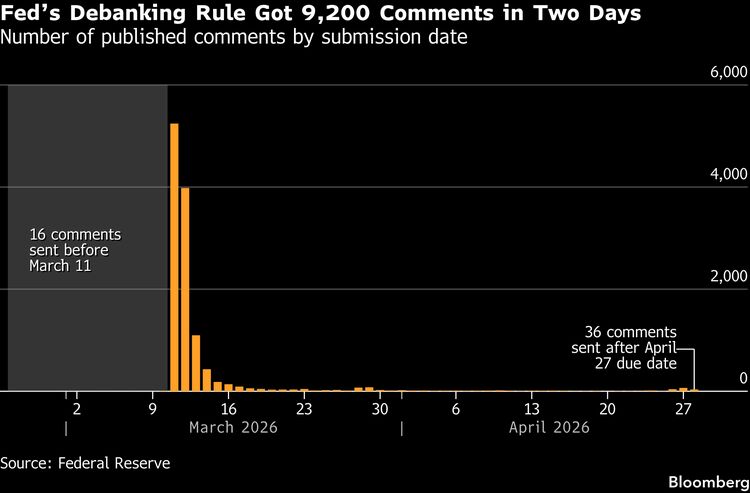

In mid-March, there was an explosion of letters filed to the Fed’s website — more than 9,200 over a couple of days. Over the months that followed, almost 2,000 people submitted signed letters, and the rest anonymously.

In high profile policy fights, special interests sometimes drum up fake comments, known as astroturfing. But when Bloomberg reached out to named commenters using contact information found independently, many responded and confirmed they had weighed in. Asked how they heard about the Fed’s proposal, they pointed to posts by people they trust on sites such as Tumblr and Threads.

A spokesperson for the Fed declined to comment.

The regulator kicked off the process a year ago, after Trump railed against debanking on the campaign trail. In its initial announcement, the Fed said it would revise references to reputation risk in supervisory materials. Still, “this does not alter the Board’s expectation that banks maintain strong risk management to ensure safety and soundness,” it said. Months later, Trump issued an executive order , demanding all watchdogs eliminate “reputation risk” regimes and “unlawful debanking.”

Since then, bank customers have complained that they’re still getting cut out of the financial system, but that firms won’t say why — leaving them in a Kafkaesque limbo. Earlier this year, Bloomberg profiled a historian in Pennsylvania whose elderly parents’ account at Citigroup Inc. was frozen for months and then closed without explanation. They received their money back weeks before his father died.

Read More: Debanking Is a Confusing Nightmare and at Risk of Getting Worse

Not all commenters understood the Fed’s proposal.

Many assumed it will go further by blocking banks from rejecting customers. In reality, it would let banks keep kicking people out if they pose a reputation risk, but with less outside oversight. (In a case of strange bedfellows, a housing advocacy group and the founder of a website known for doxing people separately expressed worries about leaving banks with that power.)

Ironically, many commenters hurled insults at Trump, apparently assuming that he is pushing to ramp up debanking, not dismantle it. So while embracing his cause, they also accused him of fascism.

In fact, when Bloomberg initially reviewed phrases declaring opposition to the Fed’s proposal, it found that roughly 1% of people fell into that camp. But the full text of their comments makes clear that more than half of those authors are confused about which direction the Fed and Trump administration are going.

“I dont want random strangers from a Bank to decide what I can or cant buy WITH MY OWN MONEY,” wrote one, mocking the Fed’s intelligence and calling its proposal out of touch, before asking, “WTF are we even doing here? Clownshow.”