What constitutes a market portfolio? SpaceX’s public listing has ignited a debate over whether index providers should speed up the addition of newly listed large companies and how fast-tracking them would affect people’s 401(k)s and broader equity performance.

If only China was having this conversation, too.

Just like the US, China’s IPO market is expected to kick into high gear. The country’s two memory chip giants ChangXin Memory Technologies Inc., or CXMT, and Yangtze Memory Technologies Co., as well as the l eading robot company Unitree Robotics, are preparing to go public on Shanghai’s STAR board, which hosts firms that align with “ national strategies ” and demonstrate “breakthrough technologies.”

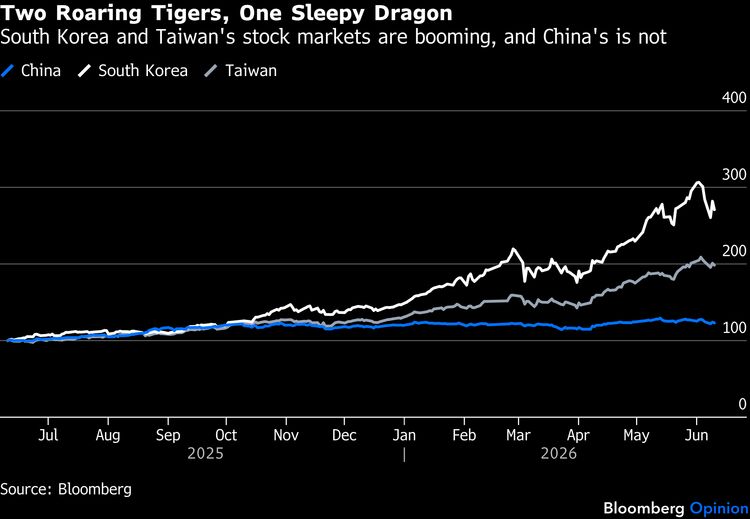

But these high-profile listings can only temporarily cover an inconvenient truth: Despite its lofty ambitions, China is not the epicenter of the artificial-intelligence trade. While South Korea and Taiwan are the world’s top-performing markets, China’s blue-chip CSI 300 Index is roughly flat this year. Economic benefits reaped from an AI-related investment boom, as evidenced by s oaring chip exports and consumer tech giants’ sizable capital spending , are not reflected in broader equity market performance.

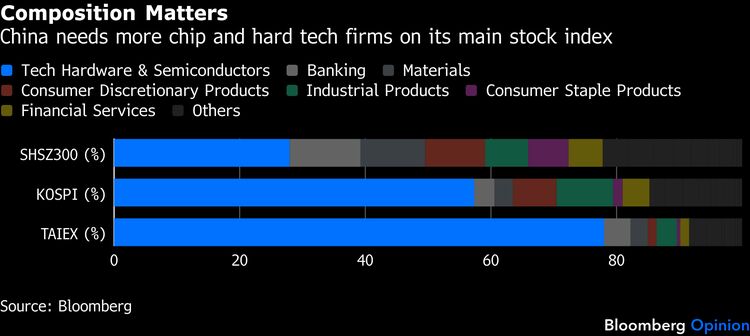

The problem is not the lack of publicly listed AI plays — but of index composition. While semiconductor and tech hardware firms account for 57% and 78% of the main indices in Korea and Taiwan, they constitute less than 30% of the Chinese benchmark.

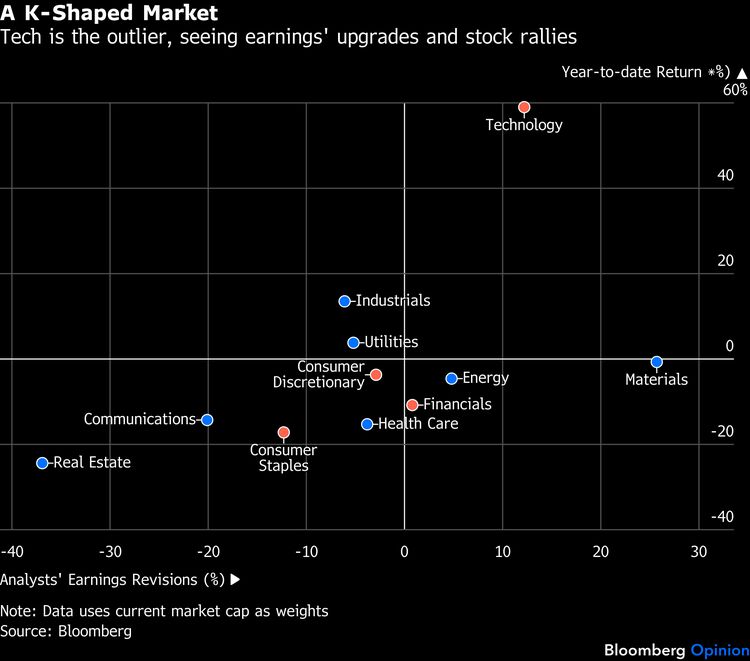

Across north Asia, companies’ robust earnings are responsible for a big chunk of the market rally. In fact, the Kospi is cheaper now than a year ago when valued on a forward earnings basis. Unfortunately for China, because of the heavy weightings of financial and consumption stocks, the CSI 300 is capped. Banks’ net interest margin is at a multi-decade low of 1.4%, and it’s no secret that consumers do not feel like spending.

Tech firms, on the other hand, are on a different trajectory. Analysts have been raising their earnings estimates, and the sector is up 59% year-to-date.

As it currently stands, China’s jazziest IPOs are unlikely to be included in the main CSI index for at least another 12 months — even if they improve their profitability or liquidity. With plans to go public on Shanghai’s STAR market, which allows more daily price fluctuations, the two memory chipmakers and Unitree will need to be listed for at least one year before becoming eligible. Meanwhile, the state-owned China Securities Index Co. meets only twice a year to review its index constituents.

Does this make sense? Once public, CXMT is expected to reach at least 1 trillion yuan ($148 billion) in market capitalization , joining the ranks of China’s 10 most valuable companies. It has also swung to profit from a loss a year earlier, and is now projected to earn at least 50 billion yuan in the first half. But this crown jewel won’t be in the national index till the end of 2027, at the earliest.

The sleepiness of the CSI 300 perhaps explains why local retail investors choose to be stock pickers, draining market liquidity with IPO oversubscription. Living in a K-shaped economy, they know that buying a broad-based index fund offers limited capital gain.

It’s time for China to consider fast-tracking the country’s mega IPOs, too. After all, President Xi Jinping can’t talk about “new productive forces” when its main stock index is flooded with anemic Old Economy companies. Sometimes, bending the rules can revive an aging stock market.

More From Bloomberg Opinion:

- Matt Levine’s Money Stuff: You Can Just Not Buy SpaceX

- SpaceX’s Capital Needs Are Out of This World: Chris Bryant

- A Trillion-Dollar Question for Memory Chipmakers: Shuli Ren

Want more Bloomberg Opinion? OPIN <GO> . Or you can subscribe to our daily newsletter .