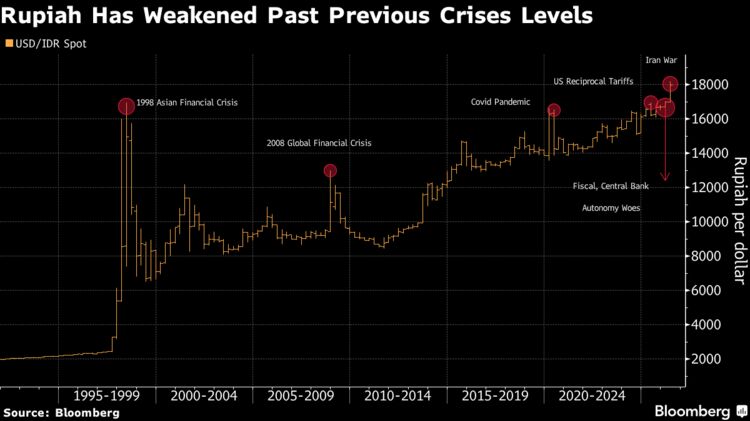

Indonesia’s rupiah — Asia’s worst-performing currency this year — has been under pressure since late 2024 when investors began reassessing the country’s fiscal outlook following the election of President Prabowo Subianto. Before this current period of volatility, the currency hadn’t traded at such weak levels since the Asian Financial Crisis of 1997-98.

Investor concerns about Indonesia have, in recent months, been compounded by the Iran war which has driven up energy prices, adding pressure to an economy that is heavily dependent on imported oil. The rupiah fell by as much as 8% in the first six months of 2026 and by early June had sunk to a record low of 18,190 against the dollar. In a surprise move to stabilize the currency, Indonesia’s central bank on June 9 increased interest rates ahead of schedule.

But with little sign of long-term relief, attention is turning to just how far the rupiah could still fall — and what that would mean for inflation, economic growth and the cost of living for Indonesia’s some 285 million people.

Why is the rupiah so weak?

The rupiah’s slide gathered pace in late 2024 after the election earlier that year of President Prabowo Subianto, who promised to roll out an ambitious social welfare agenda aimed at accelerating Indonesia’s economic growth.

Investors grew increasingly concerned about how the government would finance its flagship programs — such as a $15 billion free-lunch initiative, the rollout of about 80,000 village cooperatives and a plan to build some three million homes for low-income households — while staying within Indonesia’s legally mandated budget-deficit limit of 3% of gross domestic product. Expectations of higher government borrowing fueled worries about fiscal sustainability and debt levels, triggering capital outflows from Indonesian markets. Those outflows increased demand for foreign currencies, putting pressure on the rupiah.

Those fiscal concerns have since widened into a broader crisis of confidence. In early 2026, several global financial firms highlighted growing strains in Indonesia’s economy and capital markets, citing concerns over investability and transparency , including opaque shareholding structures and inadequate disclosures. MSCI Inc. warned in late January that it might downgrade Indonesia’s equity market to frontier status, triggering multiple trading halts and the worst two-day stocks rout in almost three decades. Moody’s Ratings and Fitch Ratings Inc. also revised their credit outlook for Indonesia to negative , while investors speculated that S&P Global Ratings could eventually follow with an outright downgrade. The developments prompted further capital outflows, deepening the rupiah’s losses.

Investor sentiment was further shaken in May when Prabowo announced the government would take direct control of exports of some of Indonesia’s most important commodities. The move fueled concerns that Southeast Asia’s largest economy was drifting toward greater state intervention. At the same time, Indonesia — a net oil importer — has faced mounting fiscal pressure from higher oil prices and the cost of fuel subsidies.

Concerns have also extended to the central bank. In June, Indonesia’s parliament passed revisions to a sweeping financial-sector law that expanded Bank Indonesia’s mandate to include supporting economic growth and gave lawmakers greater oversight of the central bank’s performance. The changes have revived long-standing worries that political considerations could play a bigger role in monetary policy, undermining confidence in the central bank’s independence and further reducing the appeal of Indonesian assets.

What are the pros and cons of a weak rupiah?

A weak rupiah creates both winners and losers, although the benefits tend to be more concentrated while the downsides are typically spread more broadly across the economy.

A weaker currency typically benefits Indonesian exporters, particularly commodity producers of coal, palm oil and nickel that sell their products in US dollars. When the exchange rate weakens, each dollar of export earnings converts into more rupiah, increasing revenues in the local currency. Government income from royalties, export taxes and income taxes linked to the natural-resources sector also tends to rise.

However, the downsides of a weak rupiah are typically felt more broadly than the benefits because many Indonesian industries rely on imported goods. When the currency weakens, imports become more expensive in rupiah terms. Even many export-oriented manufacturers depend on imported goods, such as machinery or fuel, raising production costs and offsetting much of the competitive advantage gained from a weaker exchange rate.

Businesses often pass higher import costs on to consumers, pushing up inflation, particularly for food and fuel. Rising prices erode household purchasing power and can weigh on consumer spending, the main driver of Indonesia’s economic growth. For that reason, policymakers typically try to support the rupiah, though periods of dollar strength, capital outflows and policy uncertainty can limit their ability to do so.

Are the government and central bank concerned about the rupiah?

Bank Indonesia has spent much of the last two years trying to prop up the rupiah, and its efforts intensified as the currency hit successive record lows. Governor Perry Warjiyo has said the central bank is going “all out” to stabilize the rupiah, including by intervening in markets “around the world, around the clock.”

The central bank has sold dollars from its foreign-exchange reserves to buy rupiah and traded in domestic and offshore non-deliverable forwards markets to smooth volatility and influence currency expectations. Those measures, however, have come at a cost: Indonesia’s foreign-exchange reserves fell for five straight months through May, the longest streak of declines since 2018, as the rupiah continued to weaken.

As pressure intensified in early June, the central bank delivered a rare off-cycle rate increase to bolster the currency and restore investor confidence, and the rupiah subsequently rebounded from its record low.

The government was initially more sanguine. Prabowo at one point played down the currency weakness, saying rural Indonesians do not use dollars, while Finance Minister Purbaya Yudhi Sadewa said the depreciation had been anticipated and that the budget could absorb deviations from official assumptions. But the tone shifted as the rout worsened. Prabowo later convened top economic officials, including the finance minister and Bank Indonesia governor, and called for closer policy coordination to stem the rupiah’s decline.

The government has also tightened control over exporters’ foreign-exchange earnings to boost the supply of dollars in Indonesia’s financial system. Under the policy, natural-resource exporters must keep part of their export proceeds onshore for a set period, ensuring that more foreign currency stays in domestic banks rather than being parked abroad. The measure is expected to bolster foreign-exchange liquidity and reserves, giving authorities more room to stabilize the rupiah during periods of market stress.

What’s at stake if the rupiah remains weak?

Analysts say Bank Indonesia’s measures alone may not be enough to support the rupiah over the long term if investor concerns about the government’s economic management persist. Investors want greater clarity around Prabowo’s fiscal plans and and more concrete steps to improve the attractiveness of Indonesia’s financial markets, according to Citigroup Inc. and Australia & New Zealand Banking Group Ltd.

If the rupiah remains weak, foreign investors are likely to continue offloading their Indonesian assets. Currency depreciation lowers the total returns investors get from their investments making them less attractive.

A weak rupiah could also push inflation above the central bank’s target. Rising costs are already being felt by businesses and consumers. State-owned fuel retailer PT Pertamina Patra Niaga has raised the price of non-subsidized gasoline products by about 32%, while small businesses have complained of higher costs for imported materials such as plastic. Tempeh producers across the country have also been forced to reduce production as the price of imported soybeans has risen.

Persistently higher inflation could force the central bank to raise interest rates further. Higher borrowing costs would make it more expensive for businesses to invest and expand and for households to spend, potentially slowing economic activity at a time when the government is seeking to lift growth to 6%.