Bond investors will be watching next week’s Federal Reserve meeting for signs of how quickly new Chair Kevin Warsh moves to put his own stamp on the central bank, officials at Pacific Investment Management Co. said.

Richard Clarida, a former Fed vice chair and Pimco’s global economics adviser, said investors are still trying to gauge how Warsh will approach the Fed’s communication with markets.

“Going back to the 80s, it’s understandable that when a new Fed chair comes in, there is a period maybe measured in weeks or months where you’re trying to get a sense of the regime and the communication,” Clarida said at a Pimco press event in New York Thursday. “Really the question for me is the extent to which and how Warsh puts his own stamp and puts his own focus on that communication.”

The new Fed chair lobbied for the role replacing Jerome Powell while advocating a return to a less open approach to monetary policy. During his Senate confirmation hearing in April, Warsh said, “unlike many of my colleagues past and present, I don’t believe in forward guidance.”

Bond investors are weighing possible changes including a shorter Federal Open Market Committee statement, the elimination of the dot plot and fewer press conferences by the chair. But investors would face more volatile markets if the central bank provides less guidance, acts less predictably and generates more internal debate that leads officials to dissent more regularly.

“On the margin, less communication can create a little bit more volatility and uncertainty, and that perhaps could lead to some more return through active management,” said Daniel Ivascyn, Pimco’s chief investment officer. “A Warsh Fed will be sufficiently independent in the areas that the market is most focused on, mostly rates and balance sheet policy.”

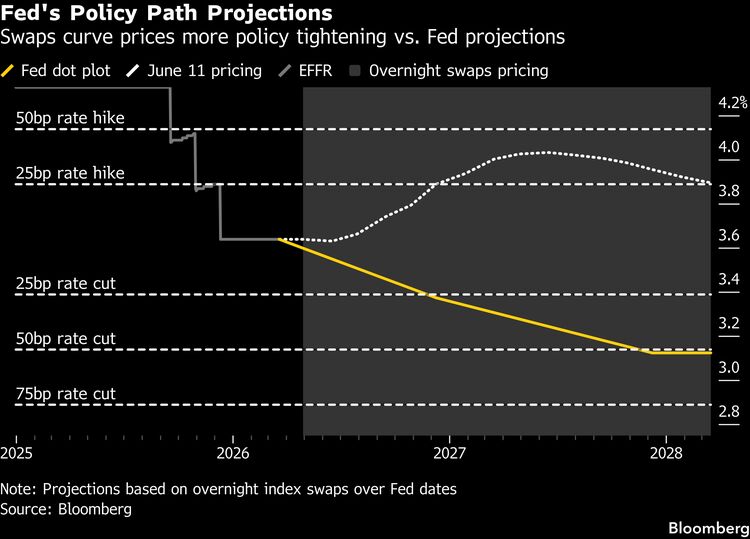

The dot plot for short-term interest rates — introduced by former Fed chair Ben Bernanke in 2012 — was designed to help guide investors in an era of ultra-low interest rates after the financial crisis.

“Forward guidance is quite important” when the funds rate is at lower levels, “so today with the funds rate where it is, from a market’s perspective it’s less important,” Ivascyn said. “When we see the dots, we talk about it a lot, it’s interesting to talk about, but you have to discount those dots heavily, first of all they are the views of individuals and there’s this concept of uncertainty and things happen.”

Highlighting how the bond market rapidly shifted from pricing in rate cuts to expecting hikes after the war in the Middle East erupted, Ivascyn said, “it didn’t take words from the Fed or an adjustment in any official language to get the two-year to sell off,” and rise toward 4.20% from around 3.4% in February.

Ivascyn cautioned that efforts to reduce front-end rates during a highly uncertain period for the global economy and inflation could work against the Fed.

“There is this realization that bringing the short rate down now doesn’t necessarily mean that very important five-or 10-year rate moves in the same direction,” and he added, “if the Fed were to cut into this period of uncertainty, you very well could get rates out the curve moving in the opposite direction, which we think would be counterproductive.”

Ivascyn said Pimco would await developments on how a Warsh Fed might seek to reduce the size of the central bank’s balance sheet, which at about $6.7 trillion has shrunk from a peak of $9 trillion in 2022. Warsh has linked a smaller balance sheet to the possibility of rate cuts.

“The balance sheet piece is something that we’re quite focused on and it can have implications for curve shape, and the performance of different maturities,” Ivascyn added. “It’s more important than what gets done on the communication side or related to the forward guidance piece.”