Wall Street has an answer for retail investors seeking to profit from elevated interest rates and dodge defaults in private credit: funds that buy collateralized loan obligations.

Firms including Franklin Templeton, Barings, Fidelity Investments and Janus Henderson have recently announced exchange traded funds that buy higher-rated portions of the vehicles known as CLOs. Collateralized loan obligations are backed by hundreds of risky corporate loans, and are set up so top-level investors in the deals are last to take losses if defaults rise.

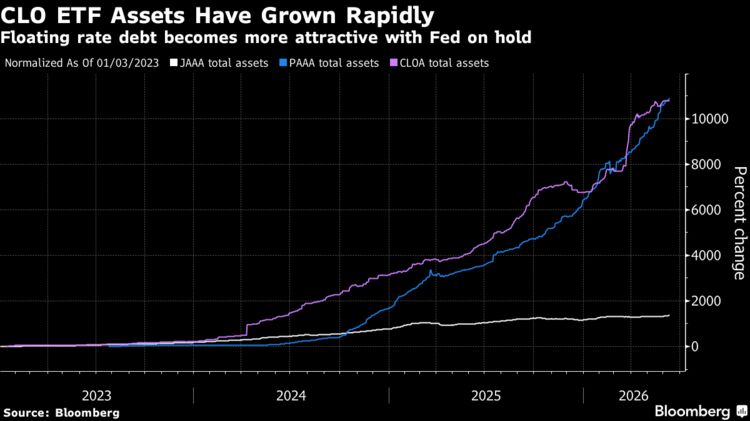

Investors have been pouring money into ETFs at the same time as they’ve been pulling money out of retail private credit funds known as business development companies, amid fears about loan defaults. Inflows into US CLO ETFs have topped $9 billion so far this year, up from nearly $7 billion during the same period last year, according to Deutsche Bank AG analysts.

Read More: Private Credit’s Resurgent Redemptions Shatter Short-Lived Calm

“If I’m looking at CLO ETF vs a BDC, CLO ETFs have become a more attractive place to get risk-adjusted yield rather than restricting my clients’ liquidity,” said Cyrus Amini, chief investment officer at Hyphen Wealth Management, adding that liquidity has also become strained for public BDCs, since investors are reluctant to sell and recognize substantial losses. “I think we’ve seen that decision play out, since the flows into these ETF funds have been very strong.”

While persistent inflation has forced central banks to keep interest rates high — bolstering yields of leveraged loans — the prolonged high borrowing costs have simultaneously weakened the balance sheets of riskier firms.

Because investment-grade CLO tranches sit higher in the capital structure, they allow investors to capture these elevated yields while forcing riskier, junior equity tranches to absorb defaults — a first wave of which some market participants warn has already begun .

That structure should, in theory, shield high-grade debt holders from underlying corporate bankruptcies. Defaults hit the bottom equity slice in the structures first because that piece “is basically 10 times levered,” said John Kerschner, global head of securitized products at Janus. “But investment grade CLOs — not at all.”

ETFs allow everyday retail investors and wealth managers to easily trade corporate debt on public exchanges. Earlier this month, Barings announced a new CLO ETF to invest at least 80% of its net assets across the CLO debt spectrum, from investment grade to the lower-ranking paper. But the loan portfolio will maintain an investment-grade profile overall, according to a filing.

“As individual retail investors get more comfortable with the characteristics and performance of CLO debt, there’s room for the market to continue to grow,” said Barings CLO portfolio manager Steve Page.

Higher Losses

CLO ETFs have been around for a few years, but the recent expansion in vehicles targeting the higher-rated portions is notable now as inflation persists due to war-driven energy shocks, cementing expectations that interest rates will remain higher for longer. For heavily-leveraged companies, that could spell trouble.

Pacific Investment Management Co. this week warned that the “credit loss cycle is upon us,” predicting in a report that there will be “significantly higher losses in lower-quality credit such as leveraged and private direct lending.”

Separately, the firm’s Chief Investment Officer Dan Ivascyn cautioned that the rapid expansion of complex credit structures is reminiscent of the buildup before the global financial crisis. Such structures securities may be winning overly generous credit ratings amid a surge in capital needs to finance AI infrastructure, he said .

Investor Sentiment

Inflows into US CLO ETFs hit $740 million around the first week of June, the largest single week of inflows since the first week of February, according to the Deutsche Bank analysts.

Much of the inflows have been into the highest-rated tranches, but BBB-rated mezzanine funds have been gaining traction in recent weeks, the bank’s analysts including Jamie Flannick said.

“When that part of the market is rallying it’s obviously a very positive sign for investor sentiment,” Flannick said.

An influx of ETF flows should spur demand for new CLOs after sales slowed this year. Issuance of broadly syndicated CLOs stands at about $58 billion, down from about $89 billion this time last year. If investor interest in these funds stays strong, issuance should accelerate in the second half, according to Flannick.

‘Compelling’ Yield

While CLO demand shows signs of resurgence, private credit is facing headwinds after retail investors asked to pull around $20 billion from those funds in the first quarter, amid concerns about valuations and software borrowers’ vulnerability to AI disruption. For some, this is making CLO ETFS more attractive — even though BDCs often pay higher yields.

“We do think that this offers a compelling yield return and total risk-adjusted return that’s an alternative to private credit,” said Jeff Masom, head of US distribution and global wealth management private markets at Franklin Templeton, which launched its YCLO ETF in June to invest in investment-grade CLO debt in the US and Europe. “I wouldn’t say this is why we brought it out, but it does play well into the current environment.”

Fidelity launched two CLO ETFs in February. The FAAA vehicle, which focuses on AAA assets, and FCLO, which focuses on lower rated portions. That same month, Janus rolled out its JA ETF to buy AA and A rated CLO tranches.

“Our message to investors is don’t try to time the market,” the firm’s Kerschner said. “It’s very, very hard to try to guess what’s going to happen. You’re still getting a good yield with a lot of diversification and a lot of liquidity.”

Click for a podcast about private lenders going back to basics from Bloomberg’s Global Credit Forum

| What to Watch |

|---|

|

Week In Review

- Pacific Investment Management Co. is warning that the “credit loss cycle is upon us” as heavy spending on artificial intelligence could widen economic outcomes and hit lower-quality borrowers. The firm’s Richard Clarida, Andrew Balls and Daniel Ivascyn said in Pimco’s latest annual secular outlook report that “the default cycle is reasserting itself, and we expect significantly higher losses in lower-quality credit such as leveraged and private direct lending.”

- SpaceX is telling investors it has lined up investment-grade ratings from three major bond graders, which could help it cut funding costs as it continues to raise financing after its $75 billion IPO. The equity offering turned the crown jewel of Elon Musk’s business empire into one of the most-valuable public companies in the world.

- Google was one of Anthropic’s earliest investors, repeatedly buying equity in the AI firm. Now it’s increasingly backstopping the financing that underpins data centers for the startup, underscoring the complex business ties among the handful of largest tech companies pouring money into AI.

-

Tencent Holdings raised nearly

$4.7 billion

from the sale of long-dated dollar and yuan bonds, marking the Chinese technology and gaming giant’s largest debt offering since 2020 as companies worldwide tap capital markets to fund AI investments.

- Banks led by JPMorgan are planning to offload about $5.3 billion in financing for software firm Qualtrics later this year in a bid to shift the hung debt off their books.

-

When Applied Digital first tapped the junk-bond market in November to fund a data center project tied to CoreWeave, it had to stomach a hefty yield to get the deal done.

Fast forward to this week

, and borrowing costs for another portion of the same project tumbled.

- Read more: Sixth Street Co-CIO Wants Exit Market for Finished Data Centers

- Institutional investors are showing faith in private credit even as retail money gets spooked, since default rates in portfolios remain low, according to Arcmont Asset Management.

-

America’s Car-Mart, a used car seller and subprime lender, is working on an

eleventh hour capital raise

to stave off a potential bankruptcy filing after a cash crunch put the company on the verge of default.

- Bankrupt auto-parts maker First Brands can make a second attempt to win court approval for a creditor vote of a proposal to raise money through lawsuits against the company’s former top officers and lenders, a judge said Monday.

- JPMorgan, Barclays and Fifth Third Bancorp won dismissal of a fraud lawsuit filed by holders of notes issued by Tricolor, the bankrupt subprime auto lender.

- Tire distributor Dealer Tire is in discussions with JPMorgan over a junk-bond sale to refinance some of its existing debt.

- Soon after selling the biggest Canadian corporate bond sale on record, Amazon.com inked another multi-billion dollar financing as spending on AI soars , getting a $17.5 billion delayed draw term loan with banks including Citigroup.

- The UK’s audit watchdog is probing accounting firms linked to Market Financial Solutions, the mortgage lender backed by multiple Wall Street banks that collapsed in February.

- Mattress maker Sleep Number filed bankruptcy with an agreement to sell the firm to one-time retail partner Sleep Country Canada after years of weak demand, mounting financial pressure and unpredictable tariffs.

- Spirit Aviation won bankruptcy court approval to start the process of selling key takeoff and landing slots at New York’s LaGuardia Airport.

On the Move

- Bank of America named George Brommer and Michail Zekyrgias co-heads of global credit, part of a broader reorganization of leadership in the firm’s fixed-income sales and trading unit.

- Canyon Partners hired former Atlas SP Partners CEO Jay Kim to lead a new asset-backed financing vehicle that will aim to originate more than $5 billion of loans annually.

- HSBC hired Spencer Jesner , formerly at Barclays , as Head of Portfolio Optimization, Americas, based in New York. He reports to Nidhi Bansal , Global Head of Financial Resource Management & Distribution for Corporate & Institutional Banking,

- Apollo is recruiting for a new European credit team focused on originating loans to small and medium-sized businesses across the region. The European Credit Company will provide financing to both private equity-backed companies and businesses without sponsors.

- Ankur Mehta is joining Citigroup ’s treasury department as head of portfolio management after leading the bank’s securitized products and credit research.

- Alantra Partners is hiring Zak Chaudary , who has been handling significant risk transfers at Deutsche Bank , as one of its leading structured finance bankers — Holger Beyer — is set to depart. Beyer is joining Revolut as head of capital markets as the digital bank pushes further into lending.

| Data Watch |

|---|

|

| NOTE: Click blue links to access Worksheets. Right click on ‘Net 5D’ column header to sort bond and loan data by price change. |