The cost to fund US equity positions is surging unexpectedly, as a combination of the AI-driven stock rally, the massive growth of leveraged ETFs and SpaceX’s $75 billion public listing tests Wall Street’s market plumbing.

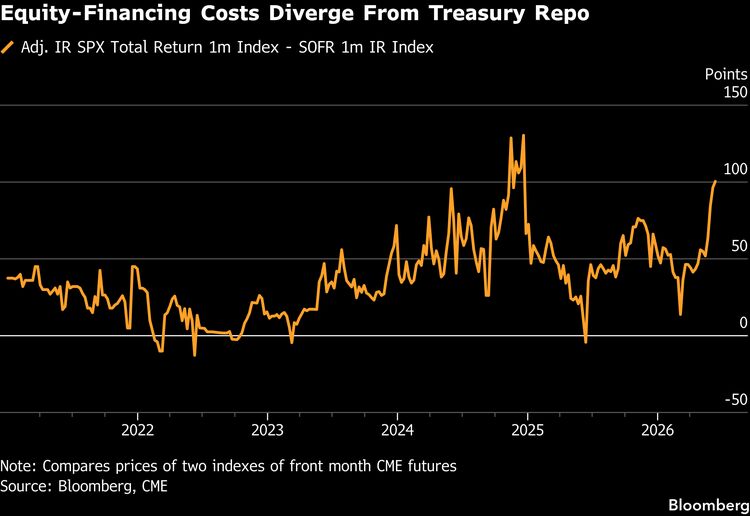

The financing spreads embedded in S&P 500 Index futures, or what an investor pays to gain economic exposure to the index without having to put up all the money, have climbed sharply over the past few weeks. That’s opened the biggest gap to Treasury financing rates since late 2024 when stocks and crypto surged after the US election.

The move is notable not just for its size, but also that it’s happening outside the year-end window , when banks typically face bigger constraints on their balance sheets. And it marks a sharp divergence from the broader funding markets: rates for borrowing against US Treasuries remain subdued. That suggests the pressure is concentrated in equity derivatives rather than being driven by a system-wide shortage of dollar funding.

“This has been one of the largest moves and richest levels that we’ve seen outside of a year-end cycle,” said Bram Kaplan, JPMorgan Chase & Co.’s head of Americas equity derivatives strategy. “The timing of it was surprising, but I think the levels are justifiable, given the record demand for equity financing and leverage at the moment.”

The supply-demand dynamics are being complicated by a slate of blockbuster IPOs that require additional balance sheet capacity from dealers. That includes Elon Musk’s SpaceX, which last week raised $75 billion in a record public debut.

“There is a finite amount of room for the financing of reserves,” said Paolo Tonucci, chief strategist and CEO of capital markets at Marex Group Plc. “The simple fact is people are trying to make room for the SpaceX IPO.”

The IPO adds to existing pressure after months of gains in stocks and a broad risk-on sentiment. Investors seeking to add exposure are using leverage to amplify returns, driving up the cost of financing positions.

The demand is intense across market participants: asset managers’ net-long futures positions are extremely high while hedge funds and systematic strategies are also heavily exposed, according to JPMorgan. This year’s rally to record highs in stocks also mechanically increased how much financing is needed for the same level of exposure.

| Read more: |

|---|

|

The IPO-related balance sheet management, as well as leverage, is driving the tightening in equity funding conditions, according to Mark Cabana, head of US interest rate strategy at Bank of America Corp.

Treasury funding is moving in the opposite direction from stocks. Repo rates have softened as cash continues to overwhelm collateral supply, fueled by heavy inflows into money-market funds and recent Treasury bill paydowns that temporarily reduced the amount of available collateral. The imbalance has kept overnight Treasury repo rates pinned near the bottom of the Federal Reserve’s target range for its policy rate.

The split is visible in market benchmarks. CME Group’s June contract for the basis on Adjusted Interest Rate S&P 500 Total Return Index futures surged to a 2026 high earlier this month. Meanwhile, the Secured Overnight Financing Rate, which tracks the cost of borrowing against Treasuries, has been trading below the Fed’s interest on reserve balances rate since the end of April.

Some $262 billion has poured into money market funds since April, pushing the total amount to an all-time high $7.89 trillion, according to Investment Company Institute data. At the same time, T-bill supply has shrunk due to paydowns after the US tax season, the Fed’s buying of short-dated debt to bolster funding conditions and the Treasury Department’s strategic purchases for cash management purposes.

Treasury’s cash balance typically rises after the mid-June corporate tax deadline, and the department is set to issue more bills to help finance widening deficits. That should boost collateral supply, which may pull funding costs higher as the market absorbs the new securities.

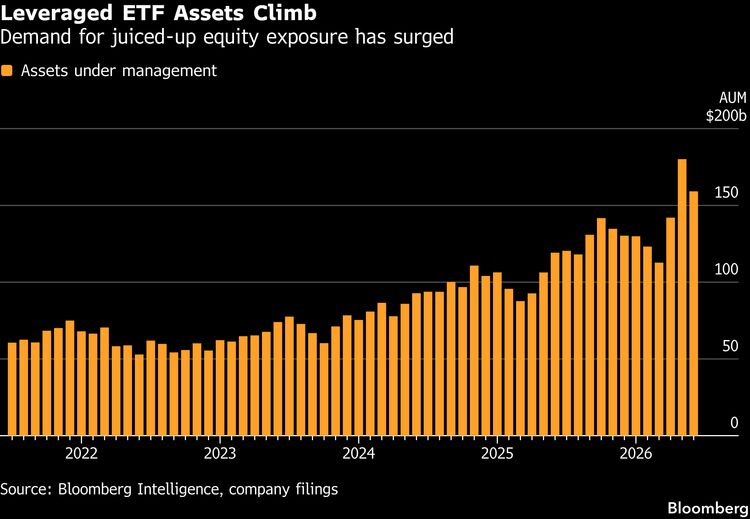

Compounding demand for equity financing is the growth of leveraged ETFs. Instead of simply buying all the stocks outright, these products use synthetic exposure through futures, swaps, options or other derivatives to achieve the desired return.

Retail investor appetite for those products has been extraordinary, particularly in the semiconductor space — and those leveraged ETFs have been expanding both in the number of new launches and in assets they’ve accumulated, according to Natasha Sibley, a portfolio manager at Janus Henderson.

“These factors together put a lot of strain on funding and pushed banks close to capacity, driving rates higher so rapidly in the last few weeks,” she said. “Each one may have been absorbed standalone but coming all together have created this funding squeeze.”

While a squeeze like this creates headaches for money managers that need leverage, it also offers an opportunity for investors sitting on cash piles: higher equity-funding costs effectively boost the returns available to those willing to lend balance sheet to the market. A typical cash-and-carry trade strategy involves purchasing stocks in the S&P 500 and selling futures against them to pocket the financing spread.

“Banks have been actively discussing equity funding trades with real money investors such as pension and sovereign wealth funds since the previous funding squeeze,” Sibley said. “Many investors will have levels in mind at which they will deploy cash. That should ease the pressure somewhat, but as always, the question is when they step in.”