Elon Musk is, famously, kind of a lot. He’s a thrice-divorced man with at least 14 children by four different women who’s spent a significant part of the past few years flirting with White nationalism and promoting a sex chatbot. He is also fabulously successful, having helped transform PayPal, Tesla and SpaceX from startups into household names — not to mention his roles in the buyout of Twitter (since rebranded as the anti-woke social network X and swallowed up by SpaceX) and the 2024 election of Donald Trump.

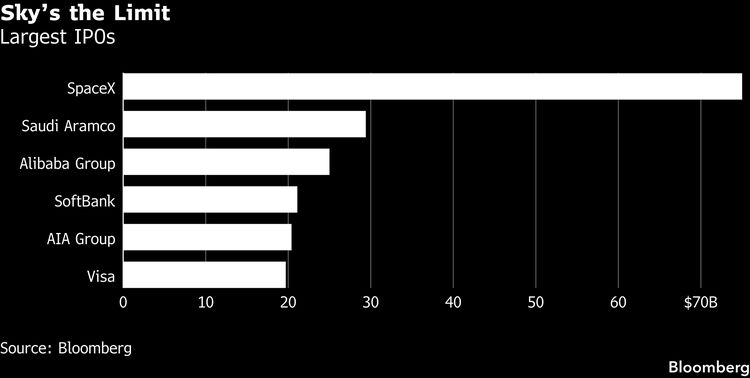

Now he is also a trillionaire . On June 12, SpaceX went public , closing with a market capitalization of $2.1 trillion, which sent Musk, who has a roughly 40% stake in the company, to a level of wealth that, as a percentage of US gross domestic product, puts him roughly on par with the richest Gilded Age monopolists . In the minds of Musk and those who bought into the largest initial public offering in history, SpaceX still has plenty of room to grow. The company’s registration statement with US financial regulators outlines three lines of business — rocket launches, satellite internet, and hardware and software for artificial intelligence — and claims that its total addressable market is $28.5 trillion, which is almost as big as America’s entire GDP. That calculation includes $370 billion for rocket launches, $1.6 trillion in satellite-related revenue and a staggering $26.5 trillion coming from the data centers Musk plans to launch into space.

The IPO filing is careful to note that the sum of those numbers doesn’t include additional revenue streams such as interplanetary travel, asteroid mining and (why not?) moon factories. It refers to the company’s market opportunity as the largest “in human history,” a phrase that appears a dozen times in the document. SpaceX immodestly credits itself with having developed “the most transformative and critical technologies in human history” — apparently putting Grok (the aforementioned chatbot) and its Starlink satellites (which provide broadband internet services on airlines and yachts) slightly ahead of breakthroughs like, say, agriculture and the wheel. A section titled “Why This Matters Now” explains that going public is important because, “We do not want humans to have the same fate as dinosaurs” and suggests the company will enable “an age of abundance with an endlessly prosperous and exciting future.”

To say it plainly, none of this makes sense, at least not according to the normal rules of business and finance. In reality, Space Exploration Technologies Corp. is a modestly sized, money-losing aerospace and telecommunications company that brought in $18.7 billion in revenue last year and lost $4.9 billion. And the losses are accelerating with Musk’s pivot toward AI: SpaceX lost $4.3 billion in the first quarter alone. By comparison, Meta Platforms Inc. — founded two years after SpaceX and, like SpaceX, investing huge sums in new AI initiatives — reported more than $200 billion in revenue in 2025 and $60 billion in profit. Meta’s market cap is more than 30% lower than that of SpaceX.

There are other issues to concern SpaceX investors. According to Musk, the company’s future depends on a gigantic experimental rocket, Starship, which will carry aloft a new generation of much larger and more advanced Starlink satellites, along with the planned orbital data centers. Musk has pitched the latter as necessary in a world of skyrocketing demand for AI and increasing concerns about electricity and land use. But Starship, which Musk first announced in 2018, has yet to reach low Earth orbit, and data centers in space are, for the moment, science fiction. In the meantime, Starlink’s margins are shrinking as it expands to poorer parts of the world and cuts prices to entice new users. A much-heralded expansion into cellphone service has been met with apathy from consumers. “We’re seeing a lot less usage than we were originally thinking,” said T-Mobile Chief Executive Officer Srini Gopalan during a recent earnings call, describing his company’s use of Starlink satellites to expand its network.

Musk’s reality distortion field has always been large, even by the standards of Silicon Valley. The entrepreneur has a knack for getting the stock market to buy into his wildest visions, no matter how unrealistic they might seem to the rest of us. Musk’s car company, Tesla , has a market cap more than five times greater than that of the next largest automotive company, Toyota Motor Corp. , even though Toyota sells six times as many cars. “If you value Tesla as a car company, you would never ever get remotely close to the valuation it trades at — same with SpaceX,” says Tim Farrar, a satellite communications consultant and analyst. “If you value SpaceX based on the Starlink business, the launch business and the reality of the AI business, then you get to valuations that are a tiny fraction of $2 trillion.” The rest is just what Farrar calls the “unknown Musk factor.”

Investors sometimes call this the “ Elon premium ,” and it has proven to be a potent economic force over the past few years. It’s also a glaring and mostly unacknowledged risk factor from which flow a host of other risks, many extending beyond SpaceX. Even if you leave aside his penchant for unconventional behavior, Musk will turn 55 at the end of June. That’s youthful by CEO standards, but Musk’s own account of his diet , exercise , sleep habits and drug use suggests he won’t be a young 55. SpaceX’s Securities and Exchange Commission filing mentions the risk that Musk might die or become disabled, but it also makes clear that the process of planning for that eventuality hasn’t even begun. It also notes that the process of identifying and recruiting a successor “could be lengthy and uncertain, and there can be no assurance that we would be able to attract or retain a suitable replacement in a timely manner or at all.”

Moreover, SpaceX is structured so that shareholders will have no leverage to get the company to disentangle itself from its founder. Musk’s supervoting shares give him more than 80% of the voting power at SpaceX and the ability to hire and fire board directors at will. Shareholder derivative suits, in which shareholders sue a board on behalf of the company, will be more or less impossible, because of Musk’s decision to move its incorporation from Delaware to Texas, a state that allows companies to set stricter limits on who can sue. SpaceX’s bylaws also force disgruntled shareholders into mandatory arbitration, which make class-action suits unlikely. Finally, the company successfully campaigned for early inclusion in index funds — Nasdaq, FTSE Russell and MSCI have all relaxed rules that would have forced it to wait set periods before joining their indexes — ensuring that a huge number of people will wind up with SpaceX in their retirement portfolio even if they don’t buy the stock directly . “Shareholders have three things they can do to hold management accountable. They can vote, they can sue, or they can sell,” says Ann Lipton , a University of Colorado law professor. “Those avenues are all gone.”

SpaceX has long been the least Musk-like part of Musk’s empire: a stable, sometimes profitable company, run by a no-drama chief operating officer for much of its 24-year history. Which is what you’d expect of a business whose chief source of revenue is government contracting. The US needs SpaceX to launch its spy satellites, to safely move astronauts to and from the International Space Station and to develop a lunar lander for NASA’s Artemis moon program. Even today, despite Starlink’s more than 10 million individual subscribers, US government contracts account for one-fifth of the company’s revenue. That’s before billions of dollars in new contracts related to Donald Trump’s planned missile defense system kick in.

Yet Musk has made clear that he now sees the company’s government work as a side quest, and that SpaceX’s future growth depends mostly on demand for AI services. For years, Department of Defense officials and members of Congress have worried about the national security implications of becoming overly dependent on Musk , given his volatility and apparent conflicts of interest. Now they might reasonably wonder if SpaceX itself is in danger of becoming distracted by the opportunities Musk sees in the AI boom.

SpaceX has few rivals in the launch business but many in AI, where it competes with Anthropic PBC and OpenAI , which both confidentially filed to go public in recent weeks. Both companies, like SpaceX, are unprofitable, and both are selling investors on a technological vision that isn’t close to being fully realized. Both have recently been valued at close to $1 trillion by private markets, and they’d likely seek even richer valuations from public investors under terms similar to those Musk has established, ensuring their founders are free from traditional oversight while pushing volatile stocks into the portfolios of retail investors and retirees. In the best-case scenario, investors will participate in a historic boom; in the worst, they will be holding the bag when the AI bubble bursts.

It’s worth saying that no one is forcing investors to bid up the valuations of SpaceX or its peers. Musk’s power, and his trillionaire status, comes from a dedicated base of small investors and day traders who have, in some cases, made huge sums of money by ignoring sober-minded attempts to value his companies. In the days before this week’s IPO, Fidelity Investments, which had generally restricted IPOs to wealthy customers with hundreds of thousands of dollars in their brokerage accounts, announced the threshold for SpaceX would be just $2,000 . Meanwhile, JPMorgan Chase & Co. CEO Jamie Dimon pitched the stock directly to the public while he boasted about “ democratizing finance .” Retail investors — who were set to account for at least 20% of the IPO, according to Bloomberg News — aren’t buying despite Musk’s baggage but because of it.

But if their instincts prove to be wrong, it won’t just be the investors who bought into Musk’s vision who’ll suffer. The fallout will hit the broader stock market, as well as the beneficiaries of the AI boom, including chipmakers, construction companies, financial firms, the Trump administration and everyone else with a stake in Musk’s AI pivot. We’re all strapped onto Musk’s rocket, whether we like it or not.