As private equity executives warn of capitulation on valuations amid a backlog of unsold assets and the Iran war unsettles the industry’s biggest backers, one Middle Eastern investor is finding opportunity.

Mubadala Investment Co.’s private equity arm has become one of the industry’s most sought-after sources of capital, capable of committing as much as $2 billion to a single transaction. Backed by the $385 billion Abu Dhabi wealth fund, the investor was involved in 16 deals in just the past three months.

In their first interview since taking charge in 2024, Co-Chief Executive Officers Camilla Languille and Luca Molinari said the vehicle’s unusual position as both a sovereign investor and a private equity-style dealmaker is allowing it to capitalize on a market increasingly starved of liquidity.

Across private markets, buyout firms are struggling to offload companies acquired during the era of cheap money. Industry executives at the SuperReturn conference in Berlin this week described parts of the market as “ constipated ,” and some warned managers may have to slash valuations , shrink funds or disappear altogether.

For Mubadala, that dislocation is creating opportunities.

“This market is becoming a productive area for our deal teams to go on the hunt,” Languille said. “We have the scale and flexibility of a sovereign investor, but we’ve got the underwriting discipline, conviction and agility of a private equity GP,” she said.

The comments come as a fragile ceasefire follows a conflict that disrupted shipping through the Strait of Hormuz, strained supply chains and cast a shadow over regional economies. Yet global investment firms continue to deepen ties with Gulf sovereign funds, which remain among the world’s most active sources of capital.

Mubadala, helmed by Khaldoon Al Mubarak, was one of the biggest backers of global deals last year with a $39 billion outlay , and has said it remains well positioned to weather fallout from the war.

Languille and Molinari expect capital deployment in their business to remain broadly consistent with prior years. The private equity division typically buys minority stakes, and is different from Mubadala Capital, which is the wealth fund’s alternative asset management arm that raises third-party capital.

The executives are now pushing the business beyond its traditional role as a capital provider, expanding into direct underwriting, minority recapitalizations and other complex transactions designed to help private equity firms unlock deals in a market where exits remain scarce.

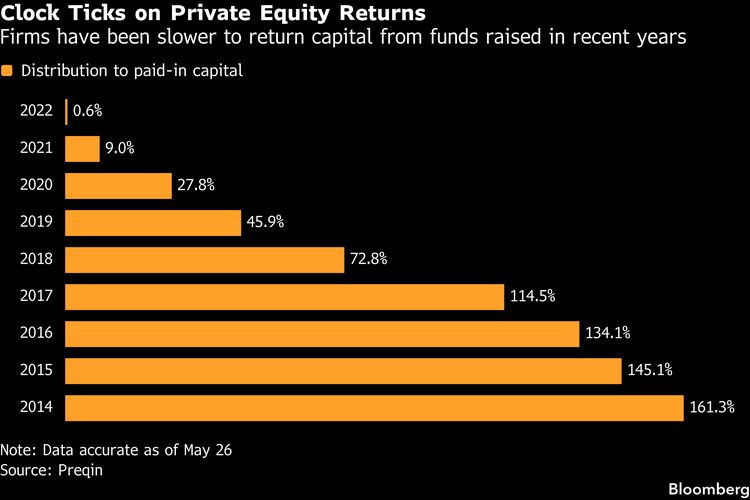

That approach is becoming more relevant: The value of sales by private equity firms is down about a fifth this year, according to data compiled by Bloomberg , frustrating investors eager to see cash returned before backing new funds.

Get the Mideast Money newsletter , a weekly look at the intersection of wealth and power in the region.

Still, activity in Mubadala’s private equity arm has accelerated this year, though much of it has stayed under the radar and the firm has disclosed just a few of its 16 transactions since March 1.

It led Athora Holding Group’s €3.5 billion capital raise alongside Mubadala unit Abu Dhabi Investment Council, and acquired a minority stake in renewable energy management suite provider Power Factors. Its model relies heavily on recycling capital through realizations and redeploying proceeds, as shown by Mubadala’s roughly $1.9 billion sell down of GlobalFoundries Inc. shares and the $4.75 billion transaction involving its minority stake in CoolIT Systems Inc., an AI data-center cooling company.

That approach encourages a relatively steady investment pace regardless of market sentiment. “When things feel great and when things feel difficult, we remain focused on finding investment opportunities,” Molinari said.

‘LP Economics, GP Mindset’

As private equity firms hold assets for longer than planned, they have turned to tactics such as continuation vehicles and minority stake sales to give investors partial liquidity, though the measures have not been enough to halt a drop in allocations to the industry.

Unlike traditional limited partners that primarily commit money to buyout funds, Mubadala increasingly underwrites transactions itself, allowing it to negotiate valuation, structure and governance terms directly.

The approach gives the fund flexibility to participate in deals ranging from classic co-investments to minority recapitalizations, general partner-led secondary transactions and direct acquisitions from private equity firms.

That capability was on display in Mubadala’s investment in healthcare payments technology company Zelis, where the fund led a minority recapitalization alongside existing owners Bain Capital and Parthenon Capital. Mubadala entered the investment at a different valuation than incumbent shareholders, and so the deal required bespoke terms designed to address differing cost bases and align interests among investors.

Those types of structures are becoming increasingly important as Mubadala targets situations where sellers seek liquidity without relinquishing control.

What began as a business that largely relied on the underwriting work of external buyout firms has evolved into a platform that conducts its own due diligence, investment analysis and portfolio management. Executives describe the model as having “LP economics and a GP mindset.”

Since Mubadala invests directly from its balance sheet rather than managing third-party funds, it does not benefit from management fees or carried interest. Investment outcomes flow directly to the sovereign fund.

“If the investment performs, we benefit. If the investment doesn’t perform, we suffer,” according to Molinari. “We own our decisions.”

Larger Checks

Mubadala’s typical equity commitment in Western markets now ranges between $500 million and $1 billion, although transactions can be as small as $200 million or as large as $2 billion.

Languille, who worked in Societe Generale SA’s M&A team and managed Virgin Group’s special situations portfolio before joining Mubadala in 2013, said the fund is “very selective” about where it deploys large checks. “It has to be in sectors, investment themes or geographies where we have high conviction.”

In Asia, where buyout markets remain less developed and large transactions are harder to find, Mubadala maintains greater flexibility around minimum investment sizes.

The sovereign fund has developed “multidimensional” relationships with many of the industry’s largest buyout firms, Languille said, often interacting with them in multiple capacities as a direct investor, co-investor, asset buyer, asset seller and fund investor.

That network, combined with Mubadala’s direct underwriting capabilities, has helped position the firm as a preferred counterparty in increasingly complex transactions.

“Not everybody has the appetite to do a large minority investment and be a solutions provider,” Molinari, who was previously a partner and managing director at Warburg Pincus, said. “That’s one of the things that the current situation in the private equity market has opened up for us.”

Another advantage lies in partner selection, with the broader sovereign wealth fund’s relationships helping identify top-performing managers across sectors and geographies. The end result is a private equity platform that owns fewer companies, commits more capital to each and plays a more active role in shaping outcomes.

“That’s been the story,” Molinari said. “Fewer, larger, more selective, more conviction. We own with intensity.”