Policymakers at the European Central Bank have just increased their benchmark interest rate by a quarter-point to 2.25%, the first change in policy in a year. While widely anticipated, the decision threatens to tip a faltering economy into recession — especially if the current bout of price increases proves unsustainable and the European energy market remains as well behaved as it has since the war in Iran began.

The surge in consumer price increases to double digits in 2022 is still fresh in the memories of euro zone rate setters. Back then, they were arguably too slow to react to the energy shock prompted by Russia’s invasion of Ukraine, only tightening policy when inflation was already accelerating more than four times faster than their 2% target. So the jump to 3.2% last month undoubtedly prompted today’s move: Once bitten, twice shy sums up the current mood in Frankfurt.

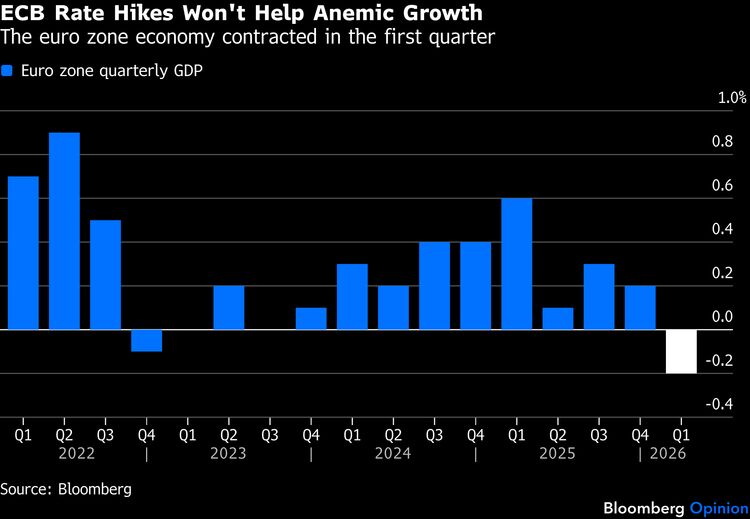

The euro zone economy is in the doldrums, with gross domestic product shrinking by 0.2% in the first quarter (albeit because of a revised slump in Ireland’s growth numbers due to the volatile contribution of large multinational firms based there). Consumer confidence in the bloc is near a three-year low, while business activity shrank at the quickest pace in two and a half years in May according to the Composite Purchasing Managers’ Index compiled by S&P Global Inc., which signaled contraction for a second consecutive month. April factory orders in Germany, the bloc’s largest economy, fell by 3.8%. With borrowing costs already elevated — at more than 3%, Germany’s 10-year bond yield has risen by half a point in the past year — Thursday’s central bank move will squeeze businesses and consumers alike.

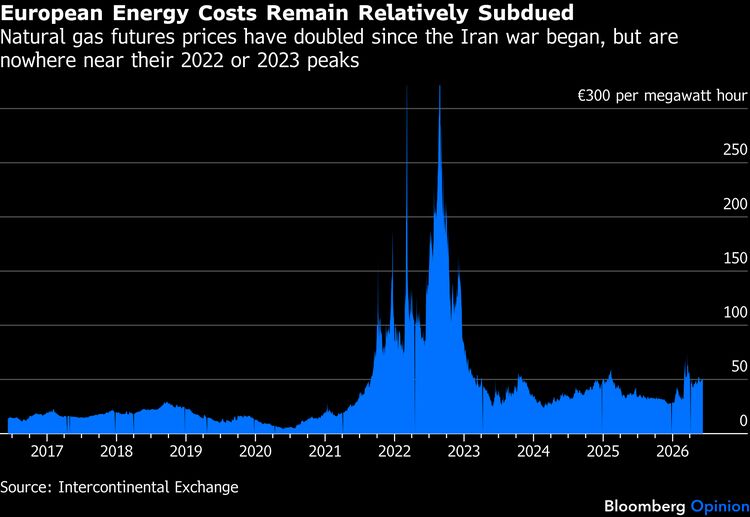

But the ECB may be fighting the last war. While the Iran conflict has disrupted about a fifth of the world’s liquified natural gas supplies, it hasn’t produced a spike in European energy prices similar to that triggered by Russia’s 2021 move to cut gas supplies to Europe ahead of its invasion of Ukraine. At around €50 ($58) per megawatt-hour, natural gas futures prices are double their pre-Iran war levels, but well below the 2022-2023 average of €87 and a far cry from the March 2022 high of €345.

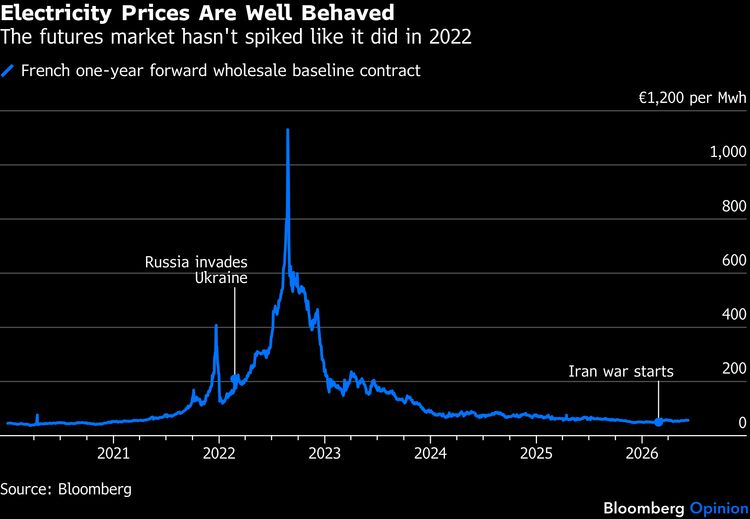

Europe’s electricity markets, meanwhile, also remain calm. France’s benchmark one-year forward contract, for example, trades at around €57 per Mwh, little changed from before the Iran war and well below the record high of €1,130 set in August 2022.

Moreover, Europe’s efforts to refill its natural gas stockpiles ahead of winter are going relatively smoothly. Since the beginning of April, the equivalent of 145 terawatts-hours of gas has been added — less than the 166 terawatts or so accumulated during the same period in 2025 but more than the 126 terawatts of 2024. By June 1, storage sites were only 41% full, compared with a 10-year average of about 53%. But at the current replenishment pace, about 70% of capacity will be reached by the end of the refill season in October — sufficient to get the region safely through winter.

The ECB rightly identified one of its 2022 problems as the supermarket trolley, which plays an outsize role in the perception of inflation. Four years ago, food prices spiked, as the war involved two breadbasket countries: Russia and Ukraine. This time, Europe isn't facing a food price shock, despite dire predictions of shortages and even famine by armchair experts. The cost of wheat, corn and soybeans, three of the most important farming commodities, is already below what it was on Feb. 27. The price of nitrogen fertilizer, a key farming input, has also fallen to prewar levels.

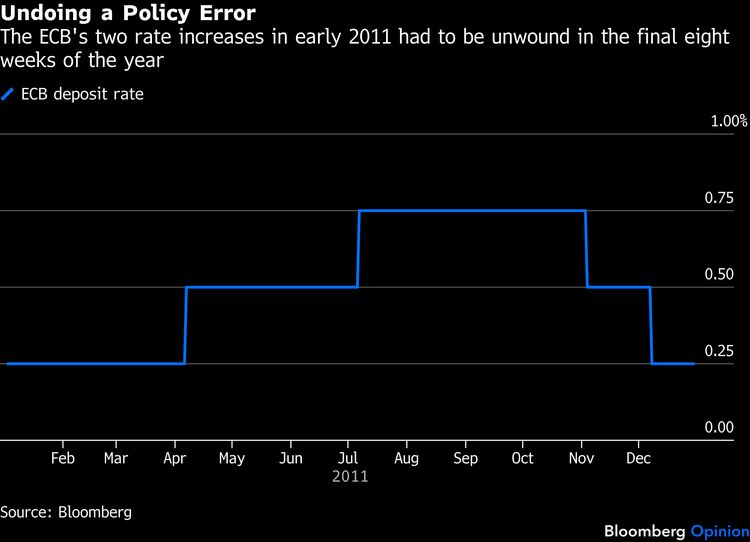

With its kneejerk response to the current headline price spike, the central bank risks repeating a policy error it committed more than a decade ago. At the end of 2010, inflation poked above the 2% target and stayed there as wounded economies were struggling to recover from the global financial crisis. In April 2011, with consumer prices rising at an annual pace of 2.6%, the ECB raised its deposit rate by a quarter-point to 0.5%; three months later, an inflation rate of 2.7% prompted a further increase to 0.75%. “We always do what is necessary to deliver price stability,” then-ECB President Jean-Claude Trichet said.

But the debt crisis that had already prompted Greece, Ireland and Portugal to seek bailout assistance from the European Union was spreading fast, with Italian and Spanish two-year yields more than doubling into the final quarter of 2011. At its November meeting, the first under new President Mario Draghi, the central bank unexpectedly cut the benchmark back down to 0.5%, followed by a further quarter-point reduction in December that marked a swift round-trip in borrowing costs.

This week’s policy decision was accompanied by a suite of new ECB forecasts. Inflation is now expected to average 3% this year and 2.3% in 2028, compared with March’s expectations for 2.6% and 2%, respectively. Policymakers cited “a higher path for energy prices, which, to some extent, is expected to feed into food, goods and services inflation.” As we’ve argued above, the central bank’s economists seem to be misjudging the outlook for energy costs, seeking to exorcise the ghosts of inflation past.

But the deterioration in the growth outlook appears more convincing, and therefore more worrying. Euro zone GDP is expected to expand by just 0.8% this year, down from the 0.9% predicted three months ago. With the economy looking anemic at best, here’s hoping Thursday’s interest-rate hike turns out to be a case of one-and-done, an effort to show willingness to act early — rather than the start of a tightening cycle.

More from Bloomberg Opinion:

- Ten Reasons Oil Is Still Below $100 a Barrel : Javier Blas

- Rationally Exuberant Markets Will Be Risking AI Mishaps in 2026: Marcus Ashworth & Mark Gilbert

- Markets May Be a Bit Too Relaxed About Inflation : John Authers

Want more Bloomberg Opinion? OPIN . Or you can subscribe to our daily newsletter .